Creative industry tax reliefs

This guide provides a clear, up‑to‑date overview of the UK’s current creative industry tax reliefs and expenditure credits, including the new audio‑visual expenditure credits introduced in January 2024.

It explains which reliefs are available, who can claim them, how much support is on offer, and the key requirements businesses must meet. The guide also addresses common misconceptions around eligibility and qualifying costs.

Despite previous challenges, the UK’s creative industries have seen renewed growth in the last two years. In 2024 the UK/Ireland box office generated £979 million, and Wicked, the biggest film of the year worldwide, was filmed at London’s Elstree studios.

Nearly ten years ago, Game of Thrones proved just how powerful High-end TV (HETV) production can be for local economies, generating over £50 million for Northern Ireland in 2018 alone. That momentum continues today: HBO’s new prequel, A Knight of Seven Kingdoms, is once again centralising the UK as a major HETV hub, with a local crew of 650 employees.

Screen content isn’t the only factor fuelling growth. The UK’s gaming industry is expanding quickly, adding £12 billion in GVA in 2025, a figure experts believe will increase in 2026 as AI and cloud gaming become more prominent.

The outlook for the UK’s creative industries is clearly promising, and as government incentives continue to adapt and expand, staying informed about the latest creative industry tax reliefs and expenditure credits is more important than ever.

This guide provides an up-to-date overview of the current creative industry tax reliefs, to help businesses in the creative sector navigate the shifting environment with confidence.

Creative industry tax reliefs (CITR) are a set of tax incentives in the UK designed to support and encourage investment in the creative industries, such as film, television, animation, video games, and theatre. The reliefs help companies offset some of their production costs by providing tax rebates or additional reductions on eligible expenses.

On 1 January 2024, the audio-visual expenditure credit (EC) replaced existing film, high-end tv (HETV), animation and children’s TV tax reliefs, and the Video Games Expenditure Credit (VGEC) replaced the Video Games Tax Relief (VGTR).

The up-to-date reliefs list is as follows:

- Film Expenditure Credit (FEC)

- High-end Television Expenditure Credit (HETV EC)

- Animation Expenditure Credit (AEC)

- Children’s Television Expenditure Credit (CTEC)

- Video Games Expenditure Credit (VGEC)

- Theatre Tax Relief (TTR)

- Orchestra Tax Relief (OTR)

- Museum & Galleries Exhibition Tax Relief (MGETR)

What audio-visual expenditure credits (AVECs) are available?

AVEC rates (from 1 January 2024)

- 39% of qualifying expenditure for animated film/TV productions and children’s TV. (For a production to qualify for these expenditure credits at least 51% or core costs should be spent on animation).

- 34% of qualifying expenditure for non-animated film/TV productions, non-children’s TV and video games.

- From 1 April 2025, films and TV programmes with a rate of 34% can claim further credit for visuals effects costs. This applies to costs incurred from 1 January 2025, and has a rate of 39% of qualifying expenditure.

Key thresholds & rules

- Expenditure threshold for HETV remains at an average of £1m per hour of slot length.

- The relief available for visual effects expenditure has increased from 34% to 39%.

- 80% cap on total core costs for all expenditure credits, except for visual effects, which is exempt.

Who can claim and when?

- The credits became available to claim after the tax period ending on or after 1 January 2024.

- The previous tax reliefs (film, television, VGTR, etc.) will remain available until 1 April 2027, allowing productions that started before 1 April 2025 to choose which scheme to claim under, while those that commenced after this date must claim expenditure credits. This also applies to VGECs.

Independent Film Tax Credit

- Available for films that have budgets of up to £15m and receive accreditation from the British Film Institute.

- Credit rate is 53% of qualifying expenditure.

- Qualifying expenditure is capped at 80% of film’s total qualifying expenditure e.g. largest taxable credit a film can claim is 6.36m (£15 million x 80% x 53%)

- Film must have started principal photography on or after 1 April 2024.

- Only expenditure incurred on or after 1 April 2024 can qualify.

What cultural reliefs are available?

Theatre Tax Relief

- 40% for non‑touring productions

- 45% for touring productions

Orchestra Tax Relief

- 45%

Museum & Galleries Exhibitions Tax Relief

- 40% for non‑touring exhibitions

- 45% for touring exhibitions

(Officially made permanent)

These tax reliefs provide an additional deduction, calculated as the lower of 80% of core expenditure or UK core expenditure. This may be used to offset taxable profits, resulting in potential corporation tax savings at a rate of 25%. Alternatively, if a loss is generated, it can be surrendered in exchange for a payable credit at the applicable relief rates.

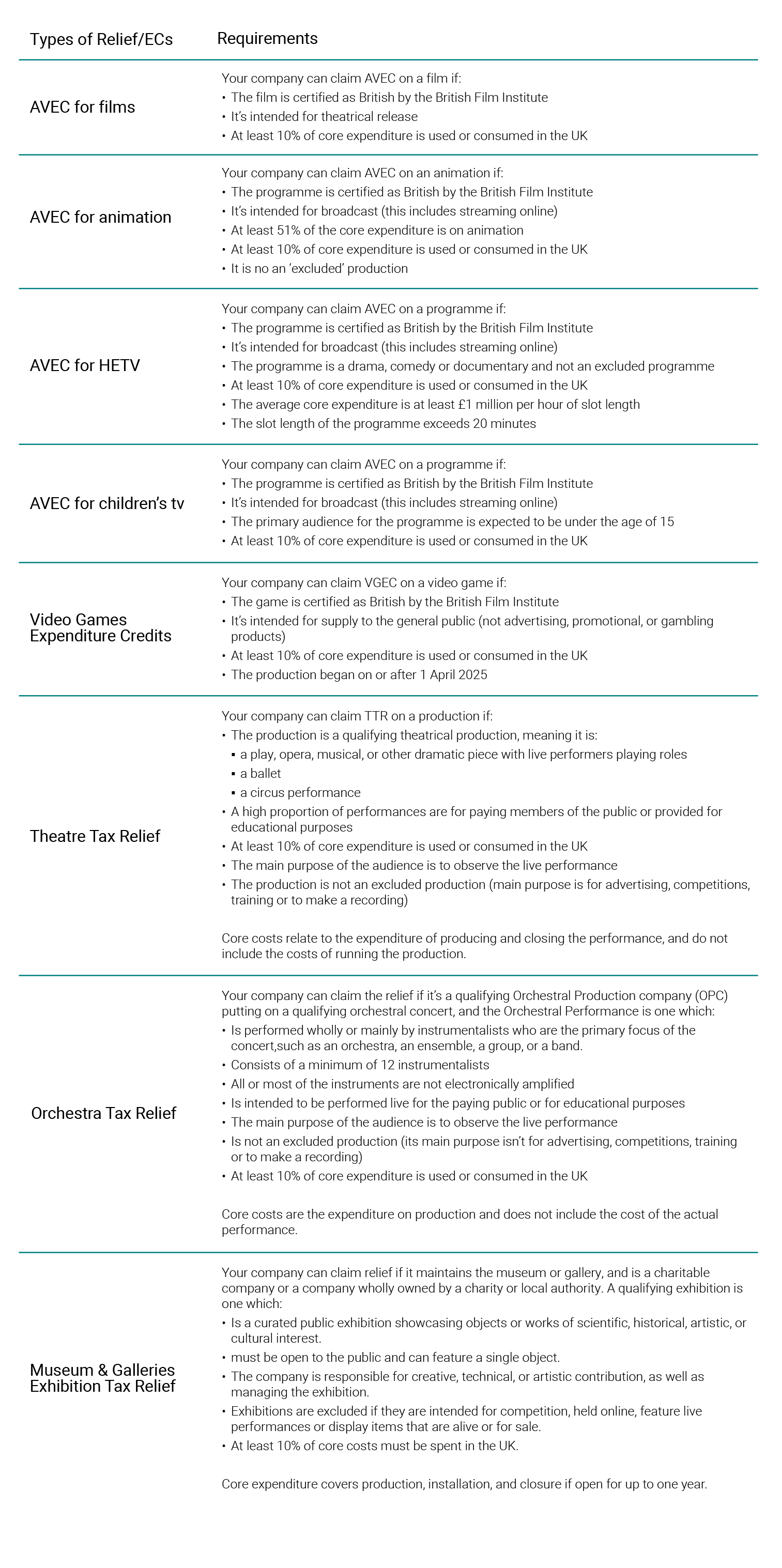

What are the specific requirements for Creative Industry Tax Reliefs?

Please note:

Companies claiming any creative reliefs, AVECs or VGECs must complete and submit an “additional information form” online before making the claim on their tax return.

For film and other productions, the claiming company must be the qualifying production company, meaning it is responsible for pre‑production, principal photography, post‑production and delivery of the final work, is actively involved in planning and decision‑making, and directly negotiates, contracts and pays for rights, goods and services.

For all creative industry expenditure credits and tax reliefs, qualifying expenditure is defined as the lower of 80% of total core costs, or the core cost of goods and services used or consumed in the UK (from 1 April 2024).

How much relief is claimed?

During the 2023/24 tax year, UK companies claimed £2.4 billion through various reliefs, encompassing both the previous audio-visual relief schemes and the newly introduced expenditure credits. This represents a 9% increase compared to the prior year. The increase was primarily attributable to higher claims for HETV Tax Relief and FTR which accounted for 46% and 22% of the total, respectively.

Number of claims by the different CITRs from 2017-18 to 2023-24

Film and Theatre consistently have the highest number of claims each year, accounting for 22% and 32% of total claims in 2023-24, respectively. Both were negatively affected by the COVID-19 pandemic, but their recovery in the years following has been different.

FTR claims have since increased following the 20% decrease in 2020-21 but only reached pre-pandemic levels in 2023-24. One of the reasons behind this is the recent increase in the number of films produced for streaming services as they typically claim HETV relief instead of FTR. This reasoning is also behind the similar trend seen in the amount of relief that has been paid out, with the difference being that the amount of relief paid out still has not returned to pre-pandemic levels.

Theatres were heavily hit by the pandemic as restrictions led to a plummet in productions. The number of TTR claims also saw a drastic decrease of over a third in 2020-21. However, 2023-24 highlights the continued strong recovery seen in 2022-23 for this industry, with the number of claims for this year increasing and remaining above pre-pandemic levels.

It is possible that the temporary increase in the relief rates of TTR contributed to this. Announced by the government in 2021 for productions that commenced production on or after 27 October 2021, it increased the tax credit rate for touring productions from 25% to 50% and non-touring productions from 20% to 45% allowing for the value of relief available to be more than doubled. This rate increase was made permanent during the 2024 Spring Budget; however, from 1 April 2025, the rates were changed to 45% for touring and 40% for non-touring productions.

Amount of relief paid for the different CITRs from 2017-18 to 2023-24

Following the pandemic, HETV relief overtook FTR in the amount of relief paid out, accounting for 46% of the total relief paid out in 2023-24. The growth of this tax relief is largely due to an increase in high-budget productions. Additionally, HETV relief’s growth over the past few years follows what has been seen by the British Film Institute regarding HETV production expenditure. The substantial growth witnessed is partially due to the increase in feature length films that are created solely for streaming services as they claim HETV relief instead of FTR.

As the VGTR was not impacted by the pandemic in the same way as the other reliefs, it has seen a steady increase in both the number and value of claims. In 2023-24, £327m of relief was paid out, a 12% increase from the previous year.

Cultural tax reliefs, defined as tax reliefs for theatres, orchestras, museums and galleries, paid out a record £339m for 2023-24, a 57% increase from the previous year. Around 77% of this was attributed to TTR, with the amount of relief paid being £261m, a 65% increase from the previous year.

The table below shows the total number and value of claims made for AVEC and VGEC up to and including 11 June 2025, by relief type, covering claims relating to both the 2023-24 and 2024-25 financial years. These figures are not uplifted to account for claims yet to be received and represent only claims that have been paid out to date. In next year’s publication, we expect to have received sufficient claims across all schemes to present data on AVEC, VGEC, and the tax reliefs, separately.

Relief type |

Relief |

Number of claims |

Amount of relief paid (£m) |

Film |

AVEC | 15 | 11 |

HETV |

AVEC | 20 | 35 |

Animation |

AVEC | 5 | 1 |

Children’s TV |

AVEC | 5 | 1 |

Video games |

VGEC | 15 | 8 |

What are some common misconceptions around claiming creative industry tax reliefs?

1. Only large productions are eligible.

Many people believe that only large-scale projects or productions are eligible for creative industry tax reliefs. CITR is available to a wide range of creative projects, including small-scale productions, independent films, animation projects, video games, and HETV. It’s not limited to big-budget productions.

2. You can claim relief for any creative project.

Many assume that any project in the creative industry is eligible for creative industry tax reliefs. Each category (e.g. film, animation, video games, etc.) has specific criteria that need to be met. For instance, organisations must comply with cultural requirements and demonstrate that no less than 10% of core expenditure relates to activities within the UK.

3. You can claim relief for any expenses.

Some believe they can claim tax relief on any expense related to the creative project. Only certain costs are eligible for creative industry tax reliefs, such as production costs, salaries, and certain qualifying overheads. Expenses such as marketing, distribution, and financing are not covered. Each tax relief program has specific rules about what costs are eligible.

Closing thoughts

As the UK’s creative sectors continue to grow, the added support provided by renewed expenditure credits and tax reliefs, can make production more accessible and financially viable. The new schemes, like the audio-visual expenditure credits and the enhanced Film Tax Credit, should give companies more opportunities than ever to reduce costs and reinvest in their work. Staying informed on these updates ensures productions can maximise available support.

Fill in the form below to speak to one of our experts for tailored support. To learn more about the video games tax reliefs and expenditure credits click here to read our more in-depth blog.

We always recommend that you seek advice from a suitably qualified adviser before taking any action. The information in this article only serves as a guide and no responsibility for loss occasioned by any person acting or refraining from action as a result of this material can be accepted by the authors or the firm.

Have a question related to creative industry tax reliefs? Contact one of our experts...

Sign up to receive exclusive business insights

Join our community of industry leaders and receive exclusive reports, early event access, and expert advice to stay ahead – all delivered straight to your inbox.

We can help

Contact us today to find out more about how we can help you