Direct and indirect costs

During some recent financial modelling conversations we’ve been having with clients, we have noticed an increasing confusion between direct and indirect costing – and their relation to fixed and variable costs.

In this article, we go ‘back to basics’ on what indirect and direct costs are, why they are important to decipher between, how they differ and relate to fixed and variable costs, and why they might not be the most commercial thing to get hung up on in financial modelling.

Not all businesses will report on, or even think in terms of, direct and indirect costs in their business, which is why it can be quite confusing when someone talks in these terms. Service businesses, for example, are less likely to categorise costs as direct or indirect, and instead fixed and variable is more likely to be the method of reporting. Direct and indirect is, instead, traditionally associated with manufacturing and product-based businesses. However, all businesses will have both direct and indirect costs, and categorising costs into those sections should (in theory) be fairly straightforward.

- Direct costs – refers to any expenditure that can be economically identified with a specific saleable cost unit.

- Indirect costs – refers to any costs which cannot be directly identified to the end product or cost category.

Example

The importance of understanding and being able to categorise costs into direct and indirect can be seen where a product director is looking to assess the viability of a new product line, and may need to source additional funding for it.

In this instance, being able to understand the step-up in costs caused by increased sales volumes, and resultant requirement for further production capacity, will help understand both the variability in investment required and whether the expansion is even viable.

This is particularly important in the current climate as we are experiencing high inflation and scarcity of resources in the supply chain in the post-COVID environment. The time value of money has never been more important, particularly on the day-to-day running of the business.

However, for growth circumstances or in the preparation for a transaction then it needs to be considered whether there is sufficient value add in reporting at this level, if it is not a matter of course.

If a business is looking to be sold, or for PE to come in for equity and allow shareholders to exit, then the investor/acquirer is unlikely to want to go into the level of granular detail that direct and indirect costs require, as they are not relevant to the situation. Instead, they are more interested in the macro view and the trends in the business.

Therefore, to the extent that they are vital to understanding the business, then yes – they are important, and time should be taken to understand the direct and indirect cost structures. However, in most circumstances where things can be reported on a variable or fixed basis, with clear assumptions on when there are ‘steps up’ in costs (as we will come on to), then the level of detail that direct vs. indirect demands is simply not commercial enough. The decision on this comes down to, as ever, what the situation is and which stakeholders are interested.

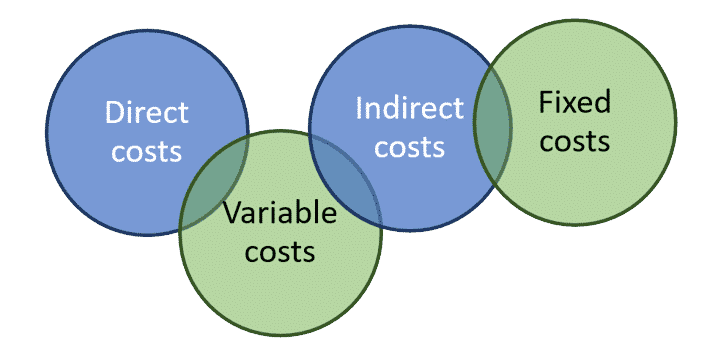

Direct and indirect vs. fixed and variable

Fixed and variable costs are different to direct and indirect. However, you will find that where there are cross-overs or similarities between them, over time these definitions have become blurred.

- Fixed costs – refers to any cost that remains constant irrespective of output. The value may change over time with inflation and growth, but the unit is fixed.

- Variable costs – refers to any cost that varies depending on the level of business activity e.g. electricity – they are variable but they can’t be calculated on a unit of production basis.

Broadly speaking, direct costs can be variable whereas indirect costs can be either fixed or variable.

There is a grey area between fixed and variable costs, a variable fixed cost so to speak. These are often referred to as ‘stepped’ costs.

For example, in the case of production led members of staff, such as factory workers (putting robotics aside) – only one member of staff can work up to a certain number of products e.g., 1 welder may be able to work on 30 products a month. If the business is forecast to produce beyond that, then it needs another welder. In this case, this type of cost is both variable and direct, as it increases with production growth and is directly attributable to a unit production cost.

Whereas if in the same scenario we consider HR, a HR employee will have a set number of employees that they can look after. If their scope of responsibility increases to 1 above that amount, then you need another HR person. In this example, the cost is variable and indirect, as it increases with production growth but cannot be directly attributed to a unit production cost. The more stepped costs within a business’s cost structure, the more volatile margins will be, and it is not until you reach the limit of a step (but not go over it) that economies of scale are realised.

This article was written by Nathan Young, Strategic Corporate Finance Manager at Price Bailey. If you are looking for support in building a financial model for your business or transaction, then please get in touch with one of the team using the form below.

We always recommend that you seek advice from a suitably qualified adviser before taking any action. The information in this article only serves as a guide and no responsibility for loss occasioned by any person acting or refraining from action as a result of this material can be accepted by the authors or the firm.

Sign up to receive exclusive business insights

Join our community of industry leaders and receive exclusive reports, early event access, and expert advice to stay ahead – all delivered straight to your inbox.

Have a question about this post? Ask our team...

We can help

Contact us today to find out more about how we can help you