Enterprise Value vs Equity Value

Whether you are making an acquisition or selling your business, sometimes the jargon used for how your business has been valued can be confusing. The two key terms used in any sale and purchase agreement in M&A transactions are Enterprise Value and Equity Value.

What is Enterprise Value?

Enterprise Value is the total value paid by the buyer for the future profits of the target in an acquisition. This headline value is intended to reflect the future earning potential of the target, and is commonly calculated by multiplying a normalised measure of profit such as EBIT or EBITDA ( Earnings Before Interest, Taxes, Depreciation, and Amortization), by a chosen pricing multiple.

Unsurprisingly, the choice of pricing multiple is highly subjective and can be influenced by many factors including potential risks, expected growth and/or anticipated synergies. Therefore, the actual multiple applied to a specific business can fluctuate far from average multiple values taken from aggregators. It is also important to understand the detail and nuances behind the deals included in generating the multiple, as they may not be representative of your deal. Nonetheless, multiples, when used correctly, are incredibly valued and used widely in valuation methodologies.

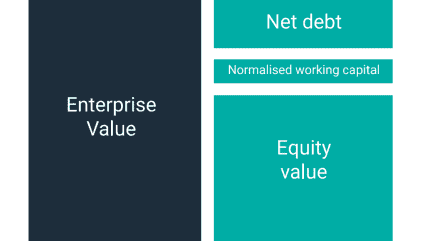

Although Enterprise Value accounts for all assets required to produce profits or revenue, it does not consider the method of financing those assets. At the time of the acquisition, the target is likely to have cash in the bank, outstanding debts, and other working capital items on their balance sheet. In most cases, buyers aim to avoid taking on any existing debts when acquiring a business, while sellers prefer not to leave behind cash unless they are compensated for it. A common solution is for both parties to agree on a cash-free and debt-free acquisition.

Another frequent assumption in deal structures is that a business will be acquired with a normal level of working capital. But once again, the choice of a ‘normal level’ of working capital can be highly contentious. Enterprise Value will therefore be subject to several adjustments to reflect the balance sheet position of the target at completion. After completing these adjustments, the result is the Equity Value.

What is Equity Value?

Equity Value is the total value a seller should receive:

Enterprise Value to Equity Value Bridge

| Item | Amount |

| Enterprise Value (Normalised EBITDA £4m x 8 multiple) | £32m |

| Add: Cash and cash-like items | £1m |

| Less: Debt and debt-like items | (£5m) |

| Add: Actual working capital | £6m |

| Less: Normal level of working capital required | (£7m) |

| <i>Working capital adjustment</i> | (£1m) |

| Equity Value | £27m |

Upon completion, conflicts may arise between the buyer and the seller concerning whether certain items should be classified as debt-like or cash-like. To help clarify these distinctions, the following table provides examples of some of the more unusual items that may fall under each category:

Cash-Like |

Debt-Like |

| Financial investments (non-core/trading) | Overdrafts, loans |

| Cash arising from exercise of share options | Invoicing discounting advances |

| Deposits released | Minority interests |

| Tax losses recoverable | Deferred consideration outstanding on past acquisitions |

| Tax recoverable on share-based payments | Staff exit bonuses |

| Committed capital expenditure |

Deferred Income is one of the most debatable items in deals. While it is in the buyer’s interest to classify deferred income as debt-like and deduct the amount from Enterprise Value (in essence leaving it behind as debt), it’s in the seller’s interest to classify deferred income as working capital. As with many items like deferred income, there is no absolute standard for classification upon completion; the appropriate treatment depends on the specific characteristics of each item and requires thorough analysis. The final classification will also be dictated by the relative bargaining power of each party in a deal.

Determining the final Equity Value can be complex and time-consuming, but using mechanisms like Completion Accounts or a Locked Box can simplify the process. Furthermore, having strong financial advice is crucial when drafting the legal contract, to ensure intentions are clear; including a pro forma calculation can also enhance clarity.

If there are relatively high levels of cash and/or low levels of debt in a business, a deal can become significantly more valuable for shareholders of the selling party. This happens because shareholders receive both the Enterprise Value and any net cash that is released from the business. However, if there are elevated levels of debt in the business, the value changing hands in a deal can be largely reduced.

Nonetheless, it is fundamentally important for business leaders involved in deals to truly understand the difference between Enterprise Value and Equity Value, as in most deals, the value paid by the buyer and the value received by the selling shareholders are different amounts.

It is important to understand the structure and terms used in a deal before you proceed. Ask your advisor, they should always be happy to explain terms and concepts to you, that’s part of our job.

For more information contact Simon Blake, Strategic Corporate Finance Partner at Price Bailey using the form below.

We always recommend that you seek advice from a suitably qualified adviser before taking any action. The information in this article only serves as a guide and no responsibility for loss occasioned by any person acting or refraining from action as a result of this material can be accepted by the authors or the firm.

Have a question about this post? Ask our team…

Sign up to receive exclusive business insights

Join our community of industry leaders and receive exclusive reports, early event access, and expert advice to stay ahead – all delivered straight to your inbox.

We can help

Contact us today to find out more about how we can help you