Consolidation requirements for UK subsidiaries of international groups

This article may be relevant to UK-headed groups that are themselves owned, wholly or in part, by one or more non-UK companies.

Such entities are often required to prepare and file consolidated financial statements in the UK, unless they correctly apply the exemption available under Section 401 of the Companies Act 2006.

Below, we outline the common exemptions from the requirement to prepare consolidated accounts, along with some practical guidance on how the rules apply.

Small UK-headed groups

If a UK-headed group and intermediate parent company are classified as small, it may qualify for an exemption from consolidation under sections 300 and 398 of the Companies Act 2006.

A group will generally be considered small if it meets two of the following thresholds for periods commencing on or after 6 April 2025:

- Net* turnover of £15 million or less/gross** turnover £18million or less

- Net total assets of £7.5 million or less/gross total assets of £9million or less

- An average of 50 or fewer employees during the period

Where a group breaches two or more of these thresholds for two consecutive years, it will no longer qualify as small. In such cases, an audit will typically become mandatory.

*Net = as per consolidated accounts

**Gross = adding together the individual accounts before deducting group transactions/balances

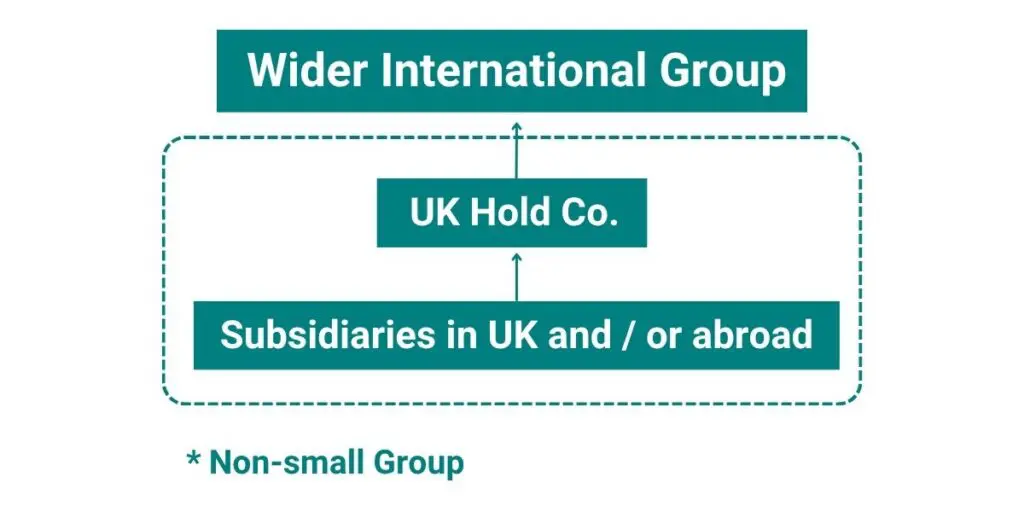

Non-small UK-headed groups

A non-small UK-headed group that forms part of a larger international group may still qualify for an exemption from preparing consolidated accounts.

The exemption under Section 401 of the Companies Act 2006 is subject to a number of strict conditions:

a. The UK holding company and all of its subsidiaries must be included in audited consolidated accounts of the wider group. These accounts must be prepared to the same balance sheet date as the UK holding company, or to an earlier date within the same financial year.

b. The consolidated accounts must be prepared in accordance with UK-adopted International Financial Reporting Standards (IFRS), or an equivalent framework. Some accounting frameworks have been designated as equivalent by the UK Treasury, currently these are the Generally Accepted Accounting Practices (GAAPs) of Canada, the People’s Republic of China, Japan, the Republic of Korea and the United States of America, EU-adopted IFRS and IFRS as issued by the IASB. However, consolidated accounts prepared under other frameworks may also meet the equivalence requirement and there is guidance on how to apply this in FRS 100.

c. The company must disclose in its individual accounts that it is exempt from the requirement to prepare and deliver consolidated accounts, and must state the name and address of the parent undertaking that prepares the group accounts.

d. To rely on the exemption from filing consolidated accounts, the UK intermediate holding company must file its own accounts together with the audited consolidated accounts of its parent. Where those accounts are not prepared in English, a certified translation must also be provided.

This exemption is not available to companies any of whose transferable securities are admitted to trading on a UK regulated market.

If you have any questions on the consolidation requirements for international subsidiaries, please contact our Audit & Assurance team using the form below. Our specialist international audit team would be happy to assist.

We always recommend that you seek advice from a suitably qualified adviser before taking any action. The information in this article only serves as a guide and no responsibility for loss occasioned by any person acting or refraining from action as a result of this material can be accepted by the authors or the firm.

Sign up to receive exclusive business insights

Join our community of industry leaders and receive exclusive reports, early event access, and expert advice to stay ahead – all delivered straight to your inbox.

We can help

Contact us today to find out more about how we can help you