Trump Tariffs

What do Trump's new global tariffs mean for UK businesses?

Change to Business and Agricultural Property Reliefs reduces risk for thousands of owner-managed estates

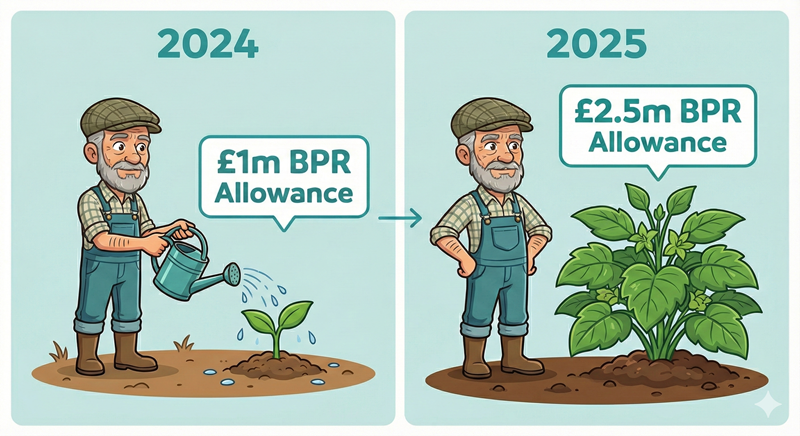

The Government has announced a major revision to its planned inheritance tax changes, increasing the threshold for both Business Property Relief (BPR) and Agricultural Property Relief (APR) from £1 million to £2.5 million, just in time for Christmas.

The move, which takes effect in April 2026, is expected to significantly reduce the number of estates affected and ease succession planning pressures for owner-managed businesses.

The move follows more than a year of pushback from across the business and rural communities, with growing concerns that the original proposals would penalise genuine trading businesses and discourage long-term investment.

Richard Grimster, Partner & Head of Tax at Price Bailey, commented:

“The news is very welcome for all owner managers and will take a level of future complexity and risk out of the estates of many; it would have been politically better to have made this announcement at the Budget last month, as it is a policy change to encourage growth and ambition to a greater extent. While the focus will immediately be on farming estates, major benefits of the revision will pass to owner managers in all sectors and simplify many estates where the assets are of a value lower than £5m. Care should still be taken when planning for the succession of family businesses, in our experience this new prospect of IHT is only one factor to consider.”

The announcement comes just before Christmas, almost a month after the Autumn Budget.

Gary Frear, Partner & Head of Equine at Price Bailey, added:

“Good news for family farms as the Government has watered down its proposal for the planned inheritance tax threshold by increasing it from £1m to £2.5m. I am sure some farmers will feel more inclined to celebrate this Christmas.

Just need wheat prices to increase and they may even treat themselves to a day off.”

While much of the public attention has been on agriculture, the revised reliefs will benefit a much wider pool of business owners, particularly those in capital-intensive sectors with valuable trading assets.

The allowance has grown since last year from £1m to £2.5m.

We always recommend that you seek advice from a suitably qualified adviser before taking any action. The information in this article only serves as a guide and no responsibility for loss occasioned by any person acting or refraining from action as a result of this material can be accepted by the authors or the firm.

What do Trump's new global tariffs mean for UK businesses?

Sarah Howarth features in Financier Worldwide’s March 2026 Global Transfer Pricing Review, exploring OECD reforms, UK reporting changes and AI in international tax.

In this blog we cover the high-level considerations, tax implications and key risks associated with a Company Purchase of Own Shares (CPOOS), including when capital treatment may be available and why careful implementation is critical.

From accounting periods beginning on or after 1 January 2026, changes to lease accounting under FRS 102 will come into force, bringing UK standards closer to IFRS 16. For professional services firms, the impact of these changes is expected to be significant. Find out more here...