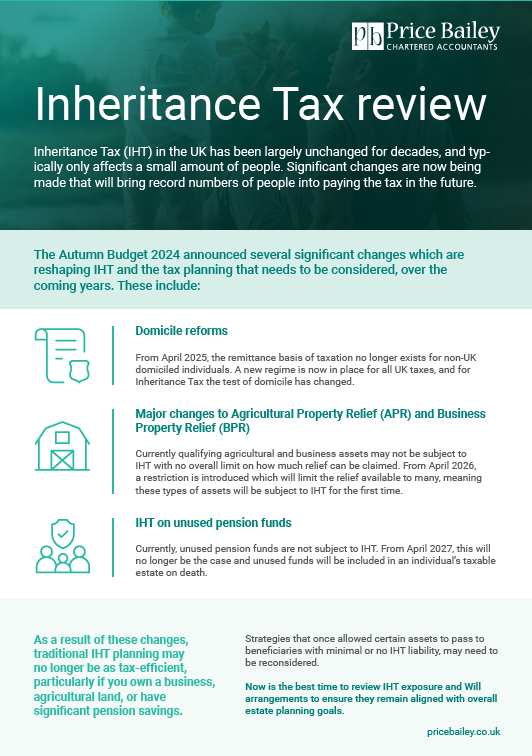

Changes to Agricultural Property Relief (APR) and Business Property Relief (BPR)

Michael Morter, a Director in Price Bailey's Tax team discusses the most recent changes to Agricultural Property Relief (APR) and Business Property Relief (BPR).

Inheritance Tax (IHT) can significantly reduce the value of your estate passed on to loved ones. HMRC statistics reveal that billions are collected annually through IHT, often from estates where little or no planning was done. Many people approach IHT indifferent, often thinking it’s inevitable or too complex to address… however, taking proactive steps can greatly reduce the amount of IHT paid and maximise what you leave behind to your beneficiaries.

Our specialist IHT and Probate team guides you through practical strategies tailored to your circumstances. The main ways to reduce your IHT liability include:

One of the simplest ways to lower IHT is by gifting assets during your lifetime, making use of exemptions and reliefs. While many are aware of basic gifting allowances, some options are often overlooked. We help clients balance making lifetime gifts while ensuring they retain sufficient resources for their own needs.

Read our blogs on Potentially Exempt Transfers (PETS) and making gifts from income for more information on lifetime gifting.

Trusts and Family Investment Companies (FICs) offer flexible ways to manage and protect wealth while maintaining some control over assets. They can be appropriate when lifetime gifting directly to beneficiaries is unsuitable or when preserving family wealth across generations is a priority. We work with legal advisers to ensure these structures align with your overall plan.

You can read more on why FICs are a popular investment vessel here.

Passing on the family home is often the most common and sensitive IHT planning question our experts receive. The residence nil-rate band (RNRB) offers an additional allowance to relieve the family home from IHT, but comes with conditions and pitfalls that many miss and is limited in value.

Giving away your family home during your lifetime can be complex due to anti-avoidance rules that apply if you continue to live in the property without paying market rent, meaning the property may still be considered part of your estate for IHT. Alternative approaches or additional steps are often required to see any IHT benefit.

Planning opportunities differ significantly between your main residence and additional properties. For second homes and buy-to-let properties, gifting during lifetime or placing assets in trusts can be effective without the same restrictions as your main residence.

Business Property Relief (BPR) and Agricultural Property Relief (APR) can dramatically reduce or eliminate IHT on qualifying assets:

Understanding whether your assets qualify requires detailed analysis, and our team can help clarify this to ensure you benefit from these valuable reliefs.

While life assurance policies do not reduce the amount of IHT payable, they are a key part of practical planning by providing funds to cover the tax liability upon death. This can protect your beneficiaries from having to sell assets to pay the tax bill. Life assurance is especially popular with older clients and is often arranged through employers or as part of estate planning strategies.

We’ve created a list of our most frequently asked questions relating to IHT to help you understand its complex world and avoid the common pitfalls.

Use our calculator to estimate your potential IHT liability and explore the impact of different planning strategies.

Our dedicated team specialises in Inheritance Tax planning for clients of all levels of wealth and complexity. Whether you live in the UK or you hold UK assets whilst living abroad, we offer expert advice tailored to your unique situation. We collaborate closely with financial advisors and solicitors to deliver a seamless, joined-up approach, often meeting with all parties together to streamline your planning process.

With the upcoming IHT changes, many people are revisiting their IHT plans… contact us today to find out more about how we can help you

Inheritance Tax in the UK has been largely unchanged for decades, and typically only affects a small amount of people. Significant changes are now being made that will bring record numbers of people into paying the tax in the future.

As a result of these changes, traditional IHT planning may no longer be as tax-efficient particularly if you own a business, agricultural land, or have significant pension savings.

We’ll keep you informed about important changes and share helpful guidance so you can stay on top of what’s relevant. Our online Insights Page is regularly updated with useful information. We also share reports, newsletters, and email alerts, and we’ll be in touch directly when something comes up that could affect you.

Big changes are happening with IHT, meaning many are having to revisit their IHT plans, contact us below to find out what’s changing and how we can support you.

Michael Morter, a Director in Price Bailey's Tax team discusses the most recent changes to Agricultural Property Relief (APR) and Business Property Relief (BPR).

Amidst the upcoming changes, our updated IHT guide will help you understand the complex world of Inheritance Tax.

Our experts unpack the key announcements of the Autumn Budget, explore the implications for businesses and individuals, and answer your questions live.

Richard Grimster, Head of Tax at Price Bailey discusses the main considerations for investing in whisky with Andrew Nelstrop, Managing Director of The English Whisky Co.

Contact us today to find out more about how we can help you