Top 5 audit findings from 24-25

Every year, as part of the statutory external audit, we report the findings of our work in our management letter presented to the Audit Committee or Governing Board.

Our audit work across the academy trust sector each year highlights recurring themes in financial management, governance and internal control. While each academy trust is unique, the issues raised often fall into consistent categories, many of which are avoidable with the right processes and oversight.

Drawing on a wide pool of findings, below are the top five most common issues raised in our academy trust audits, along with practical, actionable recommendations to strengthen compliance and financial governance.

Our historic review of 22-23 and 23-24 is archived at the bottom of this blog.

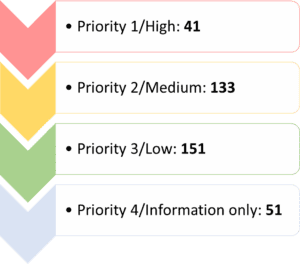

In the 24-25 year we acted for 57 academy trusts and raised a total of 376 new findings separated as follows:

What were the top 5 audit findings concerning?

- Fixed asset register issues

- Weak management accounts

- VAT compliance failures

- Governance compliance gaps (GIAS, Companies House & Website)

- Procurement and authorisation weaknesses

Weak or incomplete fixed asset registers

Across many academy trusts, our audit teams repeatedly identified:

- Fixed asset registers (FARs) not maintained throughout the year

- FARs that do not reconcile to the trial balance

- Missing or incorrect brought‑forward balances

- Failure to record disposals

- Incorrect depreciation policies applied

- Missing documentation for high-value additions

Why it matters?

The DfE Academy Trust Handbook (ATH) requires academy trusts to maintain an accurate register including cost, depreciation, net book value, additions and disposals. Section 2.6 states ‘the control framework must manage and oversee assets and maintain a fixed asset register’.

Recommendations

- Maintain the FAR monthly and include it in the month‑end close checklist

- Reconcile the FAR to the nominal ledger every month

- Record disposals promptly and use consistent asset categories

- Review useful economic lives annually to ensure compliance with the depreciation policy

- Keep documentation for all additions, especially capital projects and CIF works

- Perform termly physical verification (sample-based is fine) and record outcomes

Incomplete or non-compliant management accounts

During the 24-25 audits, it was frequently noted:

- Management accounts not shared monthly with Chair of Trustees

- Missing key statements (e.g., balance sheet, cashflow)

- High‑level reporting lacking sufficient detail for scrutiny

- Incorrect opening balances leading to inaccurate in‑year reporting

- Delays in production due to unresolved prior‑period journals

Why it matters?

Trust Boards cannot fulfil oversight responsibilities without timely, complete and reliable management reporting. The ATH requires monthly management accounts to include an income and expenditure account identifying variations to the budget, cash flow forecasts and a balance sheet.

See our blog specifically on academy trust management accounts for more detail here.

Recommendations

- Produce and circulate management accounts every month, without exception

- Include a full pack: income & expenditure, balance sheet and cashflow forecast

- Consider including relevant funds analysis for projects or restricted funds (e.g. CIF project) to allow for close monitoring

- Include a variance analysis with clear commentary

- Confirm all opening balances before the first reporting cycle

- Use a month‑end timetable with clear responsibilities and sign‑off points

- Consider a standardised Trust‑wide reporting template for consistency

VAT errors

One of the most recurrent issues across academy trusts relates to VAT, especially:

- No business vs non‑business apportionment calculation

- VAT126 forms completed incorrectly or inconsistently

- VAT returns submitted late

- Missing months or duplicated months in returns

- Lack of review or reconciliation to the control account

Why it matters?

Failure to complete VAT properly can lead to incorrect claims, clawback from HMRC, or under‑claiming funds owed to the academy trust. With HMRC increasingly performing VAT checks on academies, discrepancies increase the likelihood of a targeted compliance visit.

Recommendations

- Perform business/non‑business apportionment calculations every quarter

- Ensure VAT returns are reviewed and reconciled to the VAT control account before submission

- Use a clear checklist for preparing VAT returns to ensure completeness

- Provide refresher VAT training for finance staff at least annually. Price Bailey offer a free VAT focused webinar each year for academy trusts – details can be found on the Events section of the website.

- Consider a VAT health check review (please get in contact if you would like our specialist VAT team at Price Bailey to put together a free quote for a bespoke VAT review)

Failures in Governance Compliance (GIAS, Companies House & website)

This category is consistently one of the biggest problem areas. Common findings include:

- Get Information About Schools (GIAS) not updated within the 14‑day requirement as stated in the DfE ATH.

- Trustees recorded incorrectly or not at all

- Inconsistencies between GIAS, Companies House, and the academy trust website

- Out‑of‑date governance information on websites

- Missing registers of interests or incomplete declarations (including close family)

- Confirmation statements to Companies House filed late

Why it matters?

The DfE ATH makes it explicit that the trust board has collective accountability for ensuring compliance with regulatory, contractual, and statutory requirements. This means governance standards are not optional — they are fundamental conditions attached to public funding.

See our blog specifically relating to academy trust governance reporting requirements for more detail here.

Recommendations

- Designate a Governance Professional responsible for GIAS, Companies House and website updates

- Maintain a governance changes log to ensure deadlines are met

- Update registers of business interests annually, including close family

- Conduct a termly governance compliance check to ensure all requirements are met

Procurement, expenditure authorisation and documentation failures

This is one of the broadest and most frequent categories, covering:

- Missing purchase orders

- Purchase orders raised retrospectively

- Missing evidence of quotes

- Authorisation outside delegated limits

- Inadequate documentation (missing receipts, GRNs, approvals)

- Charge card statements not authorised

- Staff approving their own expenditure

- Unauthorised increases in credit card limits

- Policy requirements inconsistent with actual practice

Why it matters?

Weak procurement controls increase the risk of irregularity, fraud, waste, and non‑compliance with the ATH and internal financial regulations.

Recommendations

- Ensure the scheme of delegation & internal financial regulations document is up‑to‑date and followed consistently

- Require authorisation before purchase, not retrospectively

- Ensure that all required quotations are obtained and retained prior to committing expenditure, in line with the financial regulations. All quotes to be saved in a designated central location (e.g., finance drive or procurement system) and linked to the PO number.

- Maintain a list of authorised approvers for expenditure and credit cards

- Keep goods received notes (GRNs) or delivery evidence for all items in line with internal financial regulations

- Provide annual procurement and financial regulations training to all budget holders, including training on procurement thresholds and the importance of retaining evidence.

- Use audit‑trail‑friendly financial systems and discourage approvals via email or paper.

- The finance team should carry out periodic sample checks to confirm quotes are being obtained and filed correctly.

Closing thoughts

While these issues appear frequently, they are also easy to address. Academy trusts that invest in strong financial controls, clear governance processes, consistent documentation, regular training and robust month-end procedures tend to show substantial improvements year on year and significantly reduce audit findings.

Many academy trusts are reactive rather than proactive with risk registers lacking detail, controls not evaluated for effectiveness, and emerging risks such as cyber security or related-party exposure are not always fully captured. A mature risk approach helps Trustees anticipate issues before they escalate, safeguarding both public funds and educational outcomes.

An academy trust’s financial foundation is only as strong as its processes. Embedding consistency across schools (if a MAT) creates an environment where financial accuracy becomes the expectation.

Read our 23-24 audit findings here...

Each year, as part of the statutory external audit, we report the findings of our work in our management letter presented to the Audit Committee or Governing Board. We look back at some of the key audit findings from the 23-24 year.

All findings are given a priority rating based on their importance. These findings are then reported to the ESFA as part of the submission of the statutory financial statements.

In the 23-24 year we acted for 63 academy trusts and raised a total of 355 new findings separated as follows:

What were the top 5 audit findings concerning?

- Changes in governance information

- Breach of financial regulations

- Incorrect accounting treatment

- VAT treatment

- Fixed assets

Changes in governance information

The Academy Trust Handbook stipulates that academy trusts must notify the DfE of changes to their governance information via Get Information About Schools (GIAS) within 14 calendar days of the change and must publish on its website, up-to-date details of its governance arrangements. All academy trusts are also required by law to inform Companies House of any changes within 14 days.

Failure to meet these requirements results in one of the most common audit findings we report each year.

Our audit team also raised various findings relating to the register of business interests. As a reminder to all academy trusts, the ESFA Academy Trust Handbook states that;

- The trust must keep a register of any relevant business and financial interests, including governance roles in other educational institutions, for (as a minimum) members, trustees, local governors and senior employees, serving at any point over the past 12 months.

- The register must include their full names, date of appointment, term of office, date they stepped down (where applicable), who appointed them and relevant business and financial interests.

- The register must identify relevant interests from close family relationships between the academy trust’s members, trustees or local governors. It must also identify relevant interests arising from close family relationships between those individuals and employees.

- Trusts should consider whether other interests should be registered, and if in doubt should do so. Boards of trustees must keep their register of interests up-to-date at all times.

See our article here on the detailed requirements for reporting relating to GIAS, Companies House and the academy trust’s website.

Breach of financial regulations

A common deficiency we see year on year is an academy trust not following their own financial regulations or policies. Following appropriate processes and procedures put in place through the trust’s own financial regulations and policies is a key part of compliance and helps to mitigate risks.

Examples of findings raised in 23-24:

“No evidence of a tendering process being conducted despite expenditure exceeding limit per financial regulations.”

“During our review of expenditure, it was noted that purchase orders are not always raised in line with the procurement policy.”

“It was noted that for an instance of expenditure, no quotes were obtained where required per the finance regulations.”

“The majority of Trust finance manuals are significantly out of date and were last issued in December 2020.”

“Upon review of the scheme of delegation and the financial regulations, we noted that orders up to £5,000 must be authorised by the Business Manager. However, from speaking to management this does not occur in practice.”

Importance of financial regulations and scheme of delegation

Trustees and management must maintain robust oversight of the academy trust. The trust must take full responsibility for its financial affairs, and stewardship of assets, and use resources efficiently.

The governing board cannot delegate overall responsibility for the academy trust’s funds. However, it must approve a written scheme of delegation of financial powers that maintains robust internal controls. The scheme of delegation should be reviewed annually, and at the next available board meeting when there has been a change in trust management or organisational structure that would impact the effectiveness of any existing scheme of delegation.

Alcohol:

We reported 3 academy trusts of having instances of alcohol purchase in the 23-24 year and these findings were raised at the highest priority in our management letters. The ESFA guidance is clear on alcohol; “The trust’s funds must not be used to purchase alcohol for consumption, except where it is to be used in religious services.” This includes from unrestricted funds.

Incorrect accounting treatment

“We noted two instances of double counted invoices within our review of accrued expenditure. Both invoices were dated in August 2024 and were already included in trade creditors.”

“It was noted that a large proportion of trip income and expenditure relating to the year was incorrectly deferred.”

“It was noted during our testing that £626k of accruals had not been accounted for. The invoices related to capital works completed over the summer holidays.”

“We have identified an instance during our testing of purchases where the transaction date per the accounting system differs from the invoice date by 31 days.”

“During our review of non-grant income, we noted for 2 samples (out of 43) that the income received had been posted to the wrong nominal code within Sage. All income should be coded to the correct nominal.”

“We have seen that the year-end payroll creditor is not split between the balance due to HMRC and the balance due to pension providers.”

What support is available to me?

We encourage all our academy clients to contact us for support regarding accounting treatment via our free Academy Helpdesk (academy.helpdesk@pricebailey.co.uk). It is important to us that our clients feel supported throughout the year and not just during the audit period.

VAT

VAT for academies has always been a complex area and we are seeing an increasing amount of academy trusts failing short of the HMRC rules. For a lot of academy trusts we found that a business/non-business apportionment calculation was not being completed and this could give risk to a risk of overclaiming VAT.

Academy trusts who were not VAT registered and instead completing VAT126 forms often believed they were exempt from the need to do an apportionment, which is not the case. Overhead costs attributable to both business and non-business supplies must be apportioned, in a fair and reasonable manner. When completing VAT claim forms, academy trusts cannot recover VAT directly attributable to its business (i.e. trading) supplies whether taxable or exempt and cannot recover VAT relating to the proportion of overheads attributed to business supplies. There is no concept of ‘de minimis’ for this apportionment.

Academy trusts which are VAT registered must adhere to the partial exemption rules.

Academy trusts should always give consideration to the VAT implications of business and non-business supplies. We recommend any trusts who are unsure on the VAT implications to arrange for a bespoke VAT review to be undertaken by our specialist tax team who can offer guidance on the correct treatment. Please contact our Academy Helpdesk (academy.helpdesk@pricebailey.co.uk) for more information.

Fixed assets

In the 23-24 year we raised a significant number of points relating to the fixed asset register (FAR) not being maintained, the accounting system not agreeing to the FAR and incorrect capitalisation treatment.

It is an Academy Trust Handbook must to manage, oversee assets and maintain a fixed asset register. An academy trust must have its own fixed register and keep it up to date alongside the accounting system.

Last year we ran a free webinar aimed at academy trusts and maintaining the fixed asset register. A recording is available on demand. As a follow up to that session, our team of experts also wrote the following article: Fixed assets, capitalisation & maintaining the fixed asset register which is a recommended read for all our academy trusts.

Read our 22-23 audit findings here...

As Price Bailey’s audit team draw close on another year for the academies sector, we look back at some of the key audit findings from the 22-23 year.

Each year we report the findings of our work in our management letter presented to the Audit Committee or Governing Board. All findings are given a priority rating based on their importance. These findings are then reported to the ESFA as part of the submission of the statutory financial statements.

In the 22-23 year we acted for 65 academy trusts and raised a total 376 findings separated as follows:

What were the top 5 22-23 audit findings concerning?

- Related parties

- Fixed assets

- Authorisation

- Documentation

- Changes in governance information

Related parties

Audits are carrying an ever-increasing amount of regulation, especially within public funded organisations. With this in mind, the reporting of related parties is under more scrutiny than ever before and is a key area of focus for auditors and regulatory bodies alike.

In the 22-23 year we found 30% of the high priority 1 points raised were in relation to related parties. These points were either concerning a transaction that had not been correctly reported to the ESFA or business interest and declaration forms not being completed correctly.

As well as complying with the Charity SORP, academy trusts are required by the ESFA Academy Trust Handbook to report in advance all related party transactions using the ESFA’s online form.

Furthermore, ESFA approval (rather than just declaring) is required for contracts and agreements for the supply of goods or services over £40,000 effective from 1 September 2023 (historically £20,000).

We also need Trustees, Members and Key Management Personnel to declare their related parties (including close family/ connected parties) to us as their auditors. This involves the completion of a related party declaration form or access to a register maintained by the academy trust which contains this information. It is important that the names of close family are recorded, even if they do not have any substantial interests or influences. Declarations must be reviewed and updated as soon as any changes are known. All new Trustees and Members should be declaring this information before they are appointed.

Academy trusts must publish on their website, relevant business and financial interests of members, trustees, local governors and accounting officers, in line with ESFA guidance.

See our blog here on why it is important for academies to clearly disclose related parties and what the requirements are.

We host an annual webinar on related party transactions with our next one planned for May 2024. Please see our website for latest events.

Fixed assets

In the 22-23 year we raised a significant number of points pertaining to the fixed asset register not being maintained and no associated year-end adjustments being made in the finance system.

It is an Academy Trust Handbook must to manage, oversee assets and maintain a fixed asset register.

We run a free annual fixed asset training workshop with the next session due in May 2024. This session covers what and when to capitalise, ESFA capital grants, what your register may look like and how to roll it forward from the prior year, journals, disposing of an asset, new school convertors and gifted assets. This is a great opportunity to ask any questions ahead of the next audit season to ensure you do not have any recurring management letter points on maintaining the fixed asset register.

Please contact the Academy Helpdesk (academy.helpdesk@pricebailey.co.uk) or check our website for further event information.

Authorisation

In the 22-23 year nearly 15% of the findings raised were connected to authorisation of some kind.

Some examples of the type of points raised:

“During our testing of expenditure, it was noted that some purchase invoices did not have any proof of authorisation.”

“During our charge card testing it was found in one instance that the school business manager authorised their own charge card statement.”

“It was identified that three staff mileage claims were not authorised by the Head Teacher as per the Financial Regulations.”

A key part of our testing is ensuring for a sample selected, whether for charge cards, expenditure or expense claims, the processes and authorisation procedures are in line with the academy trust’s financial regulations. We often see this is not the case and thus reported as a deficiency in the academy trust’s internal control environment.

Following appropriate authorisation procedures is vital, a key part of compliance and helps to mitigate risks.

Documentation

A common deficiency we see year on year is the lack of documentation or supporting evidence, so it comes as no surprise one of the top 5 audit findings in the 22-23 year related to this.

This covers a variety of audit areas from staff ID documentation, expense claim receipts and petty cash receipts to goods received notes, purchase orders and value for money considerations.

Documentation provides a formal record of decisions agreed and in the examples above, supports work or services carried out, corroborates expenditure and ensures management are appropriately accountable for decisions made.

Changes in governance information

The Academy Trust Handbook stipulates that academy trusts must notify the DfE of changes to their governance information via Get Information About Schools (GIAS) within 14 calendar days of the change and update their website and Companies House accordingly.

When we see these various databases not being updated in a timely manner it results in an audit finding. This type of finding is one of the most recurrent points we raise each year.

See our blog here on the detailed requirements for reporting on each of these databases.

We always recommend that you seek advice from a suitably qualified adviser before taking any action. The information in this article only serves as a guide and no responsibility for loss occasioned by any person acting or refraining from action as a result of this material can be accepted by the authors or the firm.

Have a question about this post? Talk to the team now...

Sign up to receive exclusive business insights

Join our community of industry leaders and receive exclusive reports, early event access, and expert advice to stay ahead – all delivered straight to your inbox.

We can help

Contact us today to find out more about how we can help you