Contentious Tax Bulletin

Tax Investigations Partner, Andrew Park, provides a round up of the most recent and significant contentious tax news

In the May 2026 bulletin, Andrew Park, Tax Investigations Partner at Price Bailey, provides an overview of some of the most recent and significant contentious tax news, legislative changes, updates, and relevant case decisions that occurred throughout the month.

HMRC initiatives and new legislation

-

New tranche of “nudge letters” issued to claimants of Business Asset Disposal Relief (“BADR”)

As covered in the January 2026 bulletin, HMRC began the year by issuing one-to-many “nudge letters” to taxpayers who had claimed Business Asset Disposal Relief (“BADR”) in their 2024/25 Self Assessment tax returns and who, on HMRC’s records, may have exceeded the £1 million lifetime limit. HMRC has now doubled down with a further tranche of letters to new recipients in May 2026 – demonstrating that BADR, which was previously much more generous with up £10m relief, remains an active compliance focus.

The basic structure appears unchanged from the January exercise: there are understood to remain two versions of the letter – one for taxpayers whom HMRC believes had already exhausted the lifetime limit before making the 2024/25 claim, and another for those whose 2024/25 claim is said to have taken them over the limit. In each case, the taxpayer is asked either to amend the return or to contact HMRC if they consider the claim to be correct, failing which, HMRC may amend the return or open an enquiry.

As always, taxpayers in any doubt about the legitimacy of their claims should seek urgent professional advice to revisit them.

Case decisions

-

Omar Rafique v HMRC [2026] UKFTT 673 (TC)

In this case, the First-tier Tribunal (“FTT”) refused an application to reinstate an appeal that had been automatically struck out following repeated failures by the appellant to comply with tribunal directions. The underlying dispute concerned VAT liabilities and penalties which HMRC had sought to recover personally from the appellant.

The appellant had been directed to provide copies of the relevant HMRC decision letters and to set out proper grounds of appeal. Despite the issue of “unless orders” (i.e. orders requiring compliance on pain of strike-out), he failed to comply. Although a further opportunity was provided, taking account of the appellant’s ill health, the required information was still not supplied, and the appeal was struck out automatically.

The appellant subsequently applied to the FTT to set aside the strike-out and for reinstatement of the appeal. The Tribunal refused both applications, concluding that the failures to comply were serious and persistent, and that no satisfactory explanation had been provided. It also considered that, if reinstated, the appeal was unlikely to progress efficiently to a substantive hearing.

Notably, the self-represented appellant relied on submissions containing case authorities that the Tribunal found to be inaccurate or entirely fabricated, with strong indicators that they had been generated using artificial intelligence (“AI”). The Tribunal emphasised that, while there is no prohibition on using AI in preparing submissions, parties remain personally responsible for ensuring that all material put before the Tribunal is accurate and truthful.

Why this matters

This decision reinforces the strict approach taken by the Tribunal to non-compliance with procedural directions. Failure to comply with unless orders will ordinarily result in strike-out, and there is a high bar for reinstatement – which will only be granted in limited circumstances.

Of more note, it highlights once again the risks associated with unverified AI-generated material in litigation, and the need for taxpayers and advisers to ensure that all submissions are properly checked and substantiated. The Judge gave consideration to finding the appellant in contempt of court and it now seems only a matter of time – as the pitfalls of AI become better publicised – before an appellant is indeed found in contempt of court or subject to costs sanctions.

-

PGMOL v HMRC [2026] UKFTT 654 (TC) – Remitted

Upon remission from the Supreme Court, the FTT has now held that football referees engaged by Professional Game Match Officials Ltd (“PGMOL”) on a match-by-match basis were not employees for PAYE and Class 1 NIC purposes.

The Supreme Court had already decided that the individual match engagements contained the irreducible minimum of mutuality of obligation and a sufficient framework of control. The remitted issue was therefore the third stage of the Ready Mixed Concrete test: namely, whether, taking the arrangements as a whole, the other terms and surrounding circumstances were consistent with contracts of service. The Tribunal concluded they were not.

The FTT emphasised that the obligations were narrow, short-lived and heavily conditioned by choice: referees could decline appointments, make themselves unavailable and even withdraw from engagements without sanction; there was no obligation on PGMOL to provide work or on referees to accept it. Most referees had other full-time careers and the control exercised by PGMOL was largely regulatory and developmental rather than the type of managerial control usually associated with employment. Looking at the overall picture, the engagements were discrete contracts for services rather than contracts of employment.

Why this matters

This is an important reminder that satisfying mutuality of obligation and control does not, by itself, settle employment status in HMRC’s favour. Even where those threshold conditions are present, the Tribunal must still stand back and carry out the full multi-factorial assessment. For advisers, the decision is significant well beyond football. It will be cited in employment status and IR35 disputes where HMRC seeks to place heavy weight on control and the mere existence of an engagement-specific obligation to perform work.

The case also underlines the importance of distinguishing genuine managerial control from regulatory, quality assurance or framework controls, and of analysing whether the worker is really bound into an ongoing employment relationship or is instead undertaking a series of separate, voluntary assignments. In practical terms, the decision should assist taxpayers arguing that casual, ad hoc or assignment-based engagements can still fall outside employment, even where personal service and a degree of control are clearly present.

Other news and announcements

-

HMRC tax fraud warning – Bill of Exchange schemes

HMRC issued a tax fraud warning on 13 May 2026 about arrangements seeking to use “Bills of Exchange” or similar private instruments to discharge tax liabilities.

In broad terms, the schemes are marketed on the basis that the taxpayer does not pay HMRC money at all. Instead, the promoter prepares a document of notional rather than real monetary value described as a ”‘Bill of Exchange” (or uses similar language such as money orders, negotiable instruments or public trust documents) and asserts that lodging that document with HMRC somehow discharges the tax debt. The promoter will often offer to manage the process, prepare supporting affidavits and correspond with HMRC on the taxpayer’s behalf, usually for a significant fee, while presenting the arrangement as a lawful alternative payment mechanism.

HMRC has seen an increase in such attempts, particularly in the recruitment and temporary labour sector, and warns that scheme promoters are marketing these arrangements as a lawful way to wipe out tax debts or sidestep the new umbrella company rules introduced with regard to money paid to workers from 6 April 2026.

HMRC’s position is clear: it does not in any circumstances accept Bills of Exchange as payment of tax liabilities, and tax must be paid using HMRC’s normal monetary payment methods. Moreover, HMRC considers these arrangements as tax fraud rather than merely aggressive avoidance. HMRC warns that claims that such arrangements are approved by Counsel, accepted by HMRC or are capable of defeating the new umbrella company rules are simply untrue.

Taxpayers and businesses that use these schemes will still face paying the underlying tax debt, together with late payment interest, potential penalties and debt enforcement action, notwithstanding anything they have been told by promoters. Promoters will likely face criminal prosecution.

What happened in April 2026

HMRC initiatives and new legislation

- New one-to-many letters

HMRC is understood to have begun contacting:

- ‘Behind the camera’ workers in the media, reminding them of the need to carefully consider their IR35 working status and whether or not they might actually be employed rather than self-employed for tax purposes, summarising the rules and referring them to further guidance.

and

- people HMRC believe may be affected by the abolition of the non-dom regime, seeking to educate them about how the changes may affect their UK tax position.

As with all such prompts, anyone with concerns that they may not have been tax compliant or that they don’t understand their position going forward should seek professional advice.

Case decisions

-

Orsted West of Duddon Sands (UK) Ltd and Others v HMRC [2026] UKSC 12

In this saga – which twisted and turned through the lower courts – which could not agree what the law actually is, involved four windfarm companies, each owned and operated windfarms which they had constructed and duly claimed capital allowances for. The capital allowances claims included costs incurred in preliminary surveys and studies comprising visual impact assessments, wildlife impact assessments, studies on wrecks and heritage sites, noise assessments, telecoms and radar impact assessments, transport, traffic and tourism assessments, economic impact assessments, as well as oceanographic, geophysical and geotechnical studies.

HMRC contested that capital allowances were not available for the preliminary assessments and surveys, and the matter went to the First-Tier Tribunal (FTT), which allowed claims for some but not all those costs. The Upper Tribunal then disagreed and allowed HMRC’s appeal that no such costs were allowable, only for the Court of Appeal to then disagree with the Upper Tribunal and to allow most of the costs as qualifying expenditure.

All of this left the law as clear as the mud the wind turbines sit in, and it fell for the Supreme Court to decide whether any or all of the expenditure fell within the statutory definition at S11(4) of the Capital Allowances Act 2001, namely:

“The general rule is that expenditure is qualifying expenditure if—

- it is capital expenditure on the provision of plant or machinery wholly or partly for the purposes of the qualifying activity carried on by the person incurring the expenditure, and

- the person incurring the expenditure owns the plant or machinery as a result of incurring it.”

On its own analysis, the Supreme Court rejected the broader interpretative approach that the Court of Appeal had adopted and reasserted the narrower interpretation adopted by the Upper Tribunal.

In delivering the judgment, Lady Rose explained that:

- “On” sets a narrow test: Parliament used wording requiring a close connection to the plant rather than a looser “in connection with” / “relating to” / “with a view to” type test used in other tax legislation.

- The classic case authorities (especially Barclay, Curle and Ben-Odeco) support that the “limiting curve” is drawn tightly around the plant and its provision.

- While costs like transport and installation can fall within “provision”, the Court concluded that in these instances the surveys / studies were too remote: they were essentially advice / information to enable decisions about design, siting, mitigation, and consents, rather than costs of actually providing, producing, and installing the plant.

- An argument advanced by the taxpayer based on “fairness” between bespoke and off‑the‑shelf plant (i.e. that design / research is embedded in a supplier’s price) is beside the point: what matters is the nature of the purchaser’s expenditure, not the supplier’s cost build-up.

- The broader capital allowance rationale (depreciation / wear and tear) is consistent with a narrower approach, because the studies to which the claims related had at most a tangential connection to the wasting value of the physical plant.

Why this matters

- the allowable costs of providing plant (purchase, delivery, installation, and possibly some tightly connected production / installation-stage work), on the one hand

- non-allowable earlier stage costs that are better characterised as project development / design input / regulatory and environmental groundwork, on the other hand.

Other news and announcements

- Surge in VAT investigations

Newly published Freedom of Information data shows a surge of nearly one third to 11,894 in the number of VAT investigations launched by HMRC into “large” businesses in the year to 31 March 2025, over the previous year. VAT investigations into businesses as a whole surged to 110,330 from 103,790 the previous year.

This is despite HMRC making huge progress to reduce VAT non-compliance down to a current estimated loss of 5% of total VAT payable from c. 14% 20 years ago, but comes at a time of little fiscal headroom. Businesses collectively – small, medium and large – are estimated to now account for over 80% of taxes currently going uncollected, so HMRC are under enormous pressure to shift even more enforcement focus to businesses, and that is clearly happening.

All of this chimes with our experience at Price Bailey that more and more businesses are subject to compliance interventions more and more often, and is a big part of the reason we encourage our clients to take advantage of our Tax Investigations Service.

What happened in March 2026

In the March 2026 bulletin, Andrew Park, Tax Investigations Partner at Price Bailey, provides an overview of some of the most recent and significant contentious tax news, legislative changes, updates, and relevant case decisions that occurred throughout the month.

Case decisions

-

HMRC v Harte [2026] UKUT 112 (TCC)

In this case – which the taxpayer had won at the First-Tier Tribunal (“FTT”) and HMRC then sought to overturn at the Upper Tribunal – HMRC had issued discovery assessments under S29 Taxes Management Act 1970 (“TMA 1970”) for several years, each assessment aggregating multiple distinct “insufficiencies of tax” arising from different errors to which different behavioural factors applied:

- Mr Harte was self-employed and provided consultancy services (including to Tasca Tankers Limited) and had other ad hoc activities.

- HMRC issued six discovery assessments on 3 July 2018 for tax years 2009/10 to 2015/16 (excluding 2014/15, which was dealt with by an in-time enquiry and closure notice).

- The assessments comprised four categories of alleged insufficiency: (1) undeclared bank receipts; (2) personal expenditure on a corporate credit card treated as income; (3) capital allowances claimed for a vehicle; and (4) a home-office expense claim.

- HMRC argued that once any insufficiency in a year was deliberate, the whole year’s aggregated assessment was valid and the 20-year deliberate time limit applied to all included items – notwithstanding many of the items in the assessment were not deliberate omissions.

On the behavioural factors, as determined by the FTT:

(a) the bank receipt insufficiency was deliberate

(b) the capital allowance and home-office expense insufficiencies were careless

(c) the credit card insufficiency arose despite reasonable care (i.e. neither careless nor deliberate).

The Upper Tribunal agreed with the FTT and found for the taxpayer that:

- A taxpayer may show they are overcharged to the extent an assessment includes losses that do not satisfy the relevant statutory gateway and/or applicable time limit.

- S29 and S36 of TMA 1970 operate by reference to the particular insufficiency (loss of tax), not at the level of the aggregated year-wide assessment figure.

- Accordingly, amounts attributable to the credit card insufficiency (found to arise despite reasonable care) could not be included under s29(4) and had to be removed.

- Careless-only items could not be kept within the assessment for years where a separate careless assessment would have been out of time under the 6-year limit, even if the year’s assessment also contained a deliberate item within the 20-year limit.

In doing so, the Court reasoned that:

- Centrality of the particular “loss of tax”. The statutory scheme in S29 is: (1) discovery of a loss/insufficiency; (2) check whether a gateway applies; (3) assess “in order to make good … the loss of tax”. The reference in S29(4) to “the situation mentioned in subsection (1)” directs attention to the specific insufficiency discovered, not to a year-wide aggregate.

- No textual basis for “bootstrapping”. Reading S29(4) as satisfied for non-culpable items merely because another item in the same assessment is deliberate/careless would add words (such as “wholly or in part”) that Parliament did not use and would allow inclusion of losses that do not meet any gateway (where S29(5) is not relied upon).

- Time limits follow validity. S36 presupposes a valid power to assess the relevant loss under S29. HMRC’s construction wrongly gives primacy to the time-limit provision, allowing a deliberate item to “carry” other items that never satisfied S29(4) (or that satisfy it only at a lower culpability level).

- Coherence with calibrated limitation periods. Parliament set differing limits (4/6/20 years) reflecting culpability. HMRC’s approach would let a small deliberate insufficiency extend the longest limitation period to unrelated careless or non-culpable items, undermining that structure.

Why this matters

Although this decision vindicates the previous common understanding on the part of most advisers and the position previously customarily adopted by HMRC, that this wasn’t previously clearly settled law has been a nagging concern for many of us for some years. It always seemed just a matter of time before HMRC would seek to test and stretch the boundaries – and eventually HMRC did.

This welcome decision now confirms the position and sets a binding legal precedent to keep HMRC in check.

-

Hosking v HMRC [2026] UKFTT 406 (TC)

In this case heard by the FTT, the appellant appealed an Inheritance Tax (IHT) determination charging £349,309 on £1,737,236 of donations made between March 2011 and October 2016, – mainly to organisations campaigning for the UK to leave the EU. He argued the donations were exempt transfers either as (i) “normal expenditure out of income” under s.21 Inheritance Tax Act 1984 (“IHTA”), or (ii) “gifts to political parties” under S24 IHTA – as read compatibly with the ECHR via S3 Human Rights Act 1998.

In forming its decision the Tribunal was required to consider:

- S21 IHTA (normal expenditure out of income): following Bennett v IRC [1995] STC 54, “normal expenditure” means expenditure conforming with a settled pattern, shown either by (a) a pattern revealed by payments over time, or (b) a prior commitment/firm resolution regarding future spending that is then implemented. Where amounts vary, there should be a formula or standard by which payments can be quantified. The pattern must be intended to last more than a nominal period.

- S24 IHTA (gifts to political parties): exemption applies only to transfers to a qualifying political party (based on Westminster representation). In Banks v HMRC [2021] EWCA Civ 1439 the Court of Appeal explained the purpose as incentivising funding of parties with an established Westminster presence.

- ECHR (Articles 14, A1P1 and Article 10): the Tribunal applied the established Article 14 approach (including comparator analysis and justification) and considered whether limiting S24 to qualifying parties produced direct/indirect discrimination on grounds of political opinion, and whether Article 10 freedom of expression was interfered with.

With regard to the normal expenditure out of income proposition, HMRC accepted the donations were made out of income and left sufficient income to maintain the appellant’s usual standard of living, so the dispute was only whether the gifts were part of his “normal expenditure”. The Tribunal found no prior commitment or firm resolution evidenced or communicated, and no discernible settled pattern from the payments: amounts and timing fluctuated substantially, were responsive to requests and cash availability, and the appellant could not explain why particular amounts were chosen. There was no formula/standard (e.g., percentage of income or other rule) to quantify donations. The Tribunal viewed the irregularity as consistent with Nadin and insufficient to establish “normal expenditure” in the Bennett sense.

With regard to the potential political exemption, S24 / Article 14 (with A1P1): the relevant gifts were to non-party referendum campaign bodies rather than qualifying political parties, so the Tribunal concluded they did not fall within S24. Moreover, the Tribunal held there was no direct or indirect discrimination based on the appellant’s political opinion: S24 draws a line between qualifying parties and non-party organisations regardless of viewpoint, and any disadvantage arose from the mismatch between the appellant’s referendum stance and the Conservative Party’s position (and his choice to donate outside the party system), not from differential treatment of political opinions by the statute. In any event, extending S24 to non-party campaign organisations would go against the grain of the legislation and the purpose identified in Banks.

With regard to Article 10, the Tribunal found no interference with freedom of expression; the appellant was not prevented or deterred from making the donations (he donated £1.7m and said IHT was not considered in his decision-making).

Why this matters

With the increasing popularity of the gifts out of income exemption as part of many people’s Inheritance Tax planning, this case serves as a salutary reminder that simply making a stream out of ad hoc discretionary gifts out of surplus income will not of itself meet the criteria in the absence of a clear commitment, obvious pattern and some sort of common basis for the quantum. Anyone relying on this exemption should establish a rationale, make a clear future commitment and contemporaneously document that intent for their future Executors.

Other news and announcements

-

Tax treatment of Angela Rayner legal costs paid for by the Labour Party

Information obtained by The Times newspaper that the Labour Party paid out of party funds for a top tax Silk to advise Angela Rayner MP on her personal SDLT position prompted some readers to query whether that also had tax consequences in its own right.

Speaking to The Times, Price Bailey’s Andrew Park explained in relation to the provisions at S62 ITEPA 2003 that:

Tax legislation is very widely drawn so that it can catch situations where somebody receives a valuable gift — whether that’s cash, a watch, or expensive personal legal advice — in circumstances where the facts suggest that thing would not have been received were it not because of and in relation to what that person does for a living . . . Whether that’s their vocation as a jockey, a lawyer or an MP — in such circumstances, HMRC can be expected to want to assess such receipts as taxable earnings and to take a dim view of anybody who fails to disclose them.

Though Ms Rayner is not believed to have been directly employed by Labour at the time, Andrew explained that legal advice covered by the party still stood to fall within the scope of assessable income in relation to her employment out of the public purse as an MP:

It does not matter that the recipients are not directly employed by the donor — the gifts are still in relation to their employment — and the recipients are placed in the position of either having to reject the gifts or pay tax on them. Often the position can be nuanced and finely balanced because of a personal friendship or a family connection but the analysis is more clear cut where a gift is made by an institution, such as a political party, to one of its MPs.

It is understood that Ms Rayner is yet to file the relevant tax return and has until 31 January 2027 to do so and to do so accurately. However, this latest story highlights the need for people to carefully consider the tax position before accepting valuable non-cash gifts that they might want to decline rather be subject to a prohibitive amount of tax.

Although there can be a big temptation for people not to declare gifts that they cannot honestly say they would have received were it not for how they earn a living, HMRC can and do regularly investigate them – ultimately, with an eye on what they feel a Tribunal Judge would conclude the facts to be on the balance of probabilities – sourced from their occupation or sourced from something else like friendship.

What happened in February 2026

-

Francis Uzoh v HMRC [2026] UKFTT 231 (TC)

In a cautionary tale that came before the First-Tier Tribunal (“FTT”), the self-represented taxpayer sought to appeal discovery assessments made by HMRC. In most respects, this was an unremarkable case involving small sums where the taxpayer’s attempts to argue that there was no loss of tax and there were no “discoveries” of a loss of tax failed on the basis that the Judge was inclined to believe on balance that inflated claims had been made.

However, the taxpayer also sought to argue he had taken reasonable care with respect to the earliest of the assessments – which relied upon the taxpayer acting carelessly to assess back six years. Notably, the taxpayer had relied upon an online app – Tommy’s Tax – for the preparation and submission of his tax return.

As summarised in the Judge’s decision:

The Appellant’s evidence in relation to Tommy’s Tax which I accept was:

(1) He first heard of Tommy’s Tax through a friend. The friend had used Tommy’s Tax to do a ‘tax return’. Everything had gone well for the friend and there had been no issues. The Appellant also reviewed the Tommy’s Tax website and noted the testimonials.

(2) He made the Claims entirely in reliance on Tommy’s Tax: having explained to Tommy’s Tax who he was, what he was doing and where he was travelling to and from. Tommy’s Tax had assured him that what he was doing was right and correct. He believed that any mistakes in the Claims were down to Tommy’s Tax’s interpretation of the rules.

(3) He provided all the information that Tommy’s Tax asked him to provide through the App.

(4) He had only provided true and accurate information to Tommy’s Tax.

5) The Appellant did not see the Relevant Returns before they were submitted.

(6) It was after contact with HMRC that he first thought that perhaps something was not right. It is no longer possible to contact Tommy’s Tax. Additionally, the Tommy’s Tax website is down and the App has been deleted.

(7) He believed that Tommy’s Tax were legitimate as HMRC were prepared to deal with them.

However, the Judge found:

In my view a reasonable taxpayer in the Appellant’s position would have done more than wholly rely on the advice from Tommy’s Tax. For example, in circumstances where it is relatively simple to inform oneself within the PAYE context which commuting costs are recoverable as expenses to: at least consult something on the issue including legislation or HMRC guidance; or asking Tommy’s Tax to explain why the expenses were recoverable. The Appellant did neither of these things. Doing so would have prevented the Claims from being made and therefore the insufficiency of tax. Therefore, I am satisfied that the Appellant failed to take reasonable care to avoid bringing about the insufficiency of tax and was thus careless for the purposes of s29(4) TMA.

Why this matters

Although Tommy’s Tax no longer appears to be in operation, other Fintech alternatives of a similar type do still seem to exist, and doubtless more will appear, offering to help taxpayers quickly and easily deal with their tax returns at a rock bottom price, without the need for conventional professional assistance. This shows why passive reliance by taxpayers on bargain basement IT applications – without applying their own minds to the content of the returns – is not going to meet the standards of reasonable care expected by the Tax Tribunal. In this case, the taxpayer admitted that he had not even seen and reviewed the final tax returns.

The taxpayer here sought to rely, inter alia, on Hanson v HMRC [2012] UKFTT 314 (TC). Although only a lower Court FTT case, Hanson provides sound authority for taxpayers who rely on professional assistance in the preparation of their tax returns not being careless but only to the extent that those advisors are ostensibly competent, the taxpayers provide them with all relevant information and the taxpayers then check the completed tax returns themselves to the best of their ability.

-

Wood & Anor v HMRC [2026] UKFTT 00265 (TC)

In this case before the First-Tier Tribunal (“FTT”) the Appellants had purchased a large house on the banks of the Thames at Marlow for £4.5m. The house and its grounds included a section of riverside grass and a well-used public-access towpath – forming part of a national trail – running between the riverside section and the garden.

The Appellants initially paid Stamp Duty Land Tax (“SDLT”) of £586,250 upon the acquisition of the property but their accountants then filed an amended return with reduced tax of £214,500 on the basis that the full rate of SDLT did not apply because the towpath and/or the riverside area was non-residential and rendered the property as a whole “mixed use”. HMRC opened an enquiry into the amended return and sought to deny repayment of the excess tax on the basis that the original return had adopted the correct treatment and no mixed use element existed.

Both Counsel for the appellants and the HMRC litigator relied for authority on the multi-factorial methodology expounded in Upper Tribunal case HMRC v Suterwalla [2024] UKUT 188 (TC). However, the two sides put additional emphasis on the different factors which best supported their case.

With regard to the towpath, the Judge found a clear connection between the house and the towpath (and the riverside too) – them being in common ownership and contiguous. Additionally, the Judge agreed with HMRC that just because something is a public right of way and other people clearly have rights over it does not make it any less the grounds of the house. However, the Judge agreed with the taxpayers that the level of intrusion – with some 850 people using the towpath each day – rather than it simply being a public footpath, together with the lack of privacy and security was sufficient on balance – noting too, a wall between the garden and the towpath – to render it non-residential and for the appeal to succeed.

Although the appeal did not ultimately rely on it given the finding on the towpath, the Judge considered that the position with the riverside area was different. Despite a lack of privacy and security, it is for the use of the house and can be used to relax and sit on with little intrusion by the public. The householders are also free to alter its appearance and character. Therefore, on balance, he would have found – had it mattered – that the riverside is residential in character and part of the grounds of the house.

Why this matters

The case reinforces that non‑residential use need not relate to commercial exploitation. The key question is whether any part of the land fails to function as part of the residential property.

Further to this decision, the buyers of riverside homes, rural homes or shared access properties should be even more mindful to take specialist advice on the impact that any public footpaths, bridleways, shared access strips or public amenities might have on the their SDLT bill.

Other news and announcements

-

Complaints against HMRC rise to a five-year high

Complaints made by taxpayers about HMRC have surged by a fifth to reach the highest level in five years, according to data obtained by Price Bailey’s Andrew Park on behalf of the Contentious Tax Group of tax dispute professionals.

Data released under the Freedom of Information Act request reveals that HMRC received 93,589 complaints in 2024/25 up from 78,542 in 2020/21, a rise of 19.2 per cent.

The rise in complaints has gone together with an increase in the number of cases in which redress was paid by over a third (35 per cent), from 11,333 in 2020/21 to 15,304 in 2024/25. The proportion of complaints leading to redress has also risen, from 14.4 per cent to 16.4 per cent over the same period.

HMRC is being forced to accept that an ever-increasing number of taxpayers are suffering worry and distress due to its action or inaction. Every year thousands of people suffer financial loss, wasted time and needless distress because of HMRC failures to deliver the basics. The number of taxpayers compensated for “worry and distress” alone has climbed to nearly 10,000 in the most recent year. Complaints about HMRC service failings are separate from appeals against decisions about tax liabilities. Operational failings – such as incorrect coding notices, misapplied adjustments and basic processing mistakes – are major drivers of tax errors that contribute to rising complaint volumes.

According to the data, the average amount paid in cases where redress was repaid was just £125.27 in 2024/25, the lowest amount over the five-year period.

Most taxpayers complain simply to get errors corrected, yet poor service levels can cause financial losses that dwarf the modest compensation HMRC is willing to offer. Albeit, it should be noted that redress payments are expressly not intended as a substitute for the sort of large tort payments that the Courts might be prepared to award.

What happened in January 2026

HMRC initiatives and new legislation

-

Investors’ Relief

HMRC has already begun writing to people who have claimed Investors’ Relief in their latest 2024/25 tax returns upon the sale of shares in unlisted companies. There are two versions of the letters:

- one simply asking that claimants doublecheck that they meet all the qualifying criteria

and

- another stating that recipients haven’t been able to provide enough information for HMRC to allow their claims, and that they should either amend their returns to withdraw the claims, or else contact HMRC to provide further information to support the claims.

The speed with which these letters are going out shows not just the heightened attention which claims to relieve large amounts of tax now attract, but also the automation which HMRC now employs to sweep tax returns as they come in.

Full copies of the standard text can be read here:

Investors Relief – check your 2024-25 return

Investors Relief – amend your 2024-25 return

-

Business Asset Disposal Relief (“BADR”)

Similarly, HMRC has also been conducting a rapid sweep of 2024/25 Self Assessment returns to identify and perform preliminary checks on claims for Business Asset Disposal Relief and HMRC has already begun writing to individuals who its checks show have either:

- exceeded the £1m lifetime limit in making the 2024/25 claim

or

- had already exhausted the £1m lifetime limit in previous years.

Full copies of the full standard text can be read here:

BADR – overclaimed in 2024-25

BADR – fully claimed before 2024-25

-

New education letters – inclusion of cryptoassets in death estates

Further to HMRC’s efforts to heighten awareness and consideration of crypto assets, HMRC began writing to the tax agents of Executors who have recently filed IHT400 accounts asking them to check whether the deceased held any cryptoassets that might have been omitted from the assets subject to Inheritance Tax and, if so, to file Corrective Accounts.

The letters appear to be largely educational rather than intelligence driven. However, even before the new Crypto Reporting Framework (“CARF”) starts supplying information, HMRC does already have considerable data gathered through information powers or shared with it by overseas counterparts like the United States Internal Revenue Service (“IRS”). So, the risk of HMRC identifying cryptoassets that Executors have failed to identify or otherwise omitted is very real.

A copy of the full standard text can be read here:

Case decisions

HMRC v MedPro Healthcare & Ors [2026] EWCA Civ 14 – Court of Appeal reaffirms the Martland framework for late appeals

The Court of Appeal’s decision in the MedPro case marks an important return to procedural orthodoxy in the law of late tax appeals after previous confusion sown in the same case by the Upper Tribunal. The case arose out of a series of VAT penalty and personal liability notices totalling over £1m, where MedPro and related parties sought to appeal 70 days out of time. Their late appeal was refused by the First-Tier Tribunal (“FTT”), reinstated by the Upper Tribunal – whose members disagreed on whether the Upper Tribunal was even permitted to give guidance on such discretion – and ultimately escalated to the Court of Appeal.

The central issue was not the VAT dispute itself, but a procedural question – to what extent may the Upper Tribunal direct how the FTT should exercise its discretion to allow or refuse a late appeal? The Court of Appeal gave a definitive answer, holding that the Upper Tribunal is entitled to issue guidance, even where the underlying power is an “unfettered” statutory discretion. This confirms that the long‑standing three‑stage test set out by the Upper Tribunal in Martland v HMRC [2018] UKUT 178 (TCC) continues to apply, namely to:

- establish the length of delay in bringing an appeal and whether it was material,

- assess whether there was a good reason for the delay, and

- conduct a balancing exercise evaluating all circumstances, including the importance of procedural discipline and adherence to statutory deadlines.

Crucially, the Court of Appeal rejected the argument that following the Upper Tribunal guidance in Martland emphasising certain procedural factors – such as efficient litigation and respect for time limits – impermissibly fetters the FTT’s discretion. It held that highlighting important factors is not the same as removing discretion altogether. A superior court may legitimately issue guidance on the “weight” to apply to certain considerations to promote consistency. The Upper Tribunal, the Court said, had been wrong to suggest otherwise. As a result, HMRC’s appeal succeeded, and the matter is remitted to the FTT to be reconsidered under the reinstated Martland framework.

Why this matters

The decision is a clear statement that deadlines matter and should not easily be breached and that late appeals will only be admitted subject to structured and disciplined tests. Martland – now reaffirmed – remains a taxpayer‑unfriendly framework that places substantial weight on efficient case management, proportionality and finality. That said, Martland often still provides more latitude for successful appeal at the Tribunal than the narrower “reasonable excuse” criteria under which HMRC’s own statutory powers of discretion are fettered by S49 of the Taxes Management Act 1970. Now the Court of Appeal has settled the Martland tests, S49 should surely be revised for consistency so that HMRC is required to consider the same criteria rather than leaving many taxpayers with a good reason for delay, if not quite a reasonable excuse, compelled to take matters to the Tribunal before all the tests that ultimately matter can be argued.

Philip Cox & Anor v The Commissioners for HMRC [2026] UKUT 7 (TCC) – Court of Appeal overturns Upper Tribunal rejection of HMRC refusal to suspend penalties re a one-off transaction

This case concerned HMRC’s refusal to suspend penalties for careless inaccuracies arising from the taxpayers’ incorrect claims for Business Asset Disposal Relief (BADR).

Although the taxpayers briefly held 6.4% of the company’s shares, a subsequent reallocation of consideration took their holding below the 5% threshold, yet they proceeded to claim BADR in their 2019/20 returns. HMRC disallowed the relief and issued penalties, declining to suspend them on the basis that the inaccuracies arose from a one‑off event for which no meaningful suspension conditions could be set.

The taxpayers argued that HMRC had unreasonably fettered its own discretion – particularly, by applying their customary “SMART conditions” approach and by treating one‑off inaccuracies as intrinsically unsuitable for suspension. The Upper Tribunal found no such fettering. Although the FTT had erred in part of its reasoning on the statutory linkage between the original inaccuracy and future repeat behaviour, the UT held this error to be immaterial – HMRC had not applied any rigid rule and had properly considered the specific facts and the proposed suspension conditions. Those conditions – essentially promises to act prudently and to review returns with an adviser – were found to add nothing beyond what every prudent taxpayer should already be doing. On that basis, HMRC’s refusal to suspend the penalties stood.

Why this matters

Para 14(3) Sch 24 FA 2007 – which gives HMRC discretion to suspend penalties simply says:

“HMRC may suspend all or part of a penalty only if compliance with a condition of suspension would help P [a person] to avoid becoming liable to further penalties under paragraph 1 for careless inaccuracy.”

The decision is helpful to taxpayers in making clear that no statutory requirement can be inferred by HMRC into this paragraph that would automatically prevent penalties relating to one-off events from being suspended. Advisers have had this argument with HMRC since the penalty suspension regime first came into being.

However, the decision concludes that suspension of penalties by HMRC should not be the norm in cases involving one‑off transactions. To secure suspension, taxpayers must identify specific, measurable and genuinely preventative conditions capable of reducing the risk of recurrence. Where the inaccuracy stems from a unique set of circumstances – such as a bespoke transaction or a one‑time restructuring – there will usually be no practical suspension conditions that meet the statutory test.

What happened in December 2025

HMRC initiatives and new legislation

-

HMRC education letters warning advertising agencies about making R&D claims

During the month, HMRC mass mailed advertising agencies with pre-emptive warning letters warning them about the remote feasibility of them successfully making R&D claims.

In an effort to get ahead of unscrupulous R&D boutiques, HMRC has been monitoring their activities and has become aware that some of them are still targeting advertising companies with bogus suggestions they can qualify for R&D relief. In HMRC’s own words:

“Most claims aren’t eligible. This is because they’re usually based on:

- normal day-to-day work – creating, adapting or duplicating digital billboards, banners, adverts, or client websites, on a regular basis

- making adverts or products with a client’s brand or desired specifications without advancing a field of science or technology

- developing tools that collect customer data and analyse their behaviour

- using existing technology, for example VR, to showcase a client’s products

- developing bespoke software platforms by utilising already existing knowledge or capability to combine software features already existent within software

- buying ‘off the shelf’ e-commerce platforms, customer relationship management systems or dataset management tools, and adapting them to suit the business.”

As with all R&D claims, projects must aim to achieve an advance in overall knowledge or capability in a field of science or technology, not just within the company in question. They must aim to resolve an area of scientific or technological uncertainty in a way that can’t just be readily deduced by a competent professional with existing knowledge. In that context, the limited scope of advertising companies to make valid claims speaks for itself.

A copy of the full standard text can be read here: Claims for R&D tax relief

Case decisions

-

WM Morrison Supermarkets Ltd v HMRC [2025] UKFTT 1542 (TC)

This issue heard by the First-Tier Tax Tribunal (“FTT”) – rather than by the High Court as misreported by most of the Press – centred on whether Morrisons’ “cool-down” rotisserie chickens should be treated as hot food for VAT purposes under Note 3B, Group 1, Schedule 8 of the Value Added Tax Act 1994.

Morrisons argued that:

- the chickens were zero-rated because they were often eaten cold or reheated at home – to the extent they might still be sold heated that was incidental not deliberate;

- HMRC had previously indicated this treatment was acceptable and were therefore bound by legitimate expectation.

HMRC maintained that the chickens were sold in heat-retentive packaging in foil-lined bags labelled “Caution: hot product” and remained well above ambient temperature for up to two hours after cooking, meeting the statutory definition of hot food.

The FTT found for HMRC, concluding that:

- the packaging was specifically designed to retain heat and prevent leakage of hot fluids;

- the chickens were not on a cooling trajectory that would make them “incidentally hot” when sold;

- Morrison’s had no legitimate expectation – HMRC had not expressed a clear, unambiguous and unqualified view on the matter – moreover, Morrisons had failed to fully disclose all material information, including that the chicken was routinely taken off sale after two hours when still well above ambient temperature.

Why this matters

This ruling lands Morrisons with a £17m+ tax bill before interest and penalties and reinforces HMRC’s interpretation of the “pasty tax” rules introduced in 2012 – which were relaxed after an outcry to exclude items such as Greggs pasties sold at ambient temperature – but which do still apply VAT to hot takeaway food sold above ambient temperature or placed above ambient temperature into heat-retentive packaging.

What happened in November 2025

Contentious Tax Roundup – What Happened in November 2025

In the November 2025 bulletin, Andrew Park, Tax Investigations Partner at Price Bailey, provides an overview of some of the most recent and significant contentious tax news, legislative changes, updates, and relevant case decisions that occurred throughout the month.

Autumn Budget 2025

A number of new measures were announced on 26 November 2025 to help close the tax compliance gap. These included:

-

New whistleblower scheme

With immediate effect from Budget Day, potential informers may be eligible for payments from HMRC of between 15% and 30% of the tax received where the tax recovered is over £1.5m.

However, unlike the US – which inspired the new UK initiative – informers will have no absolute entitlement to a reward just by meeting fixed criteria.

In the first instance, claimants will have to demonstrate that they don’t fall foul of an extensive list of exclusions – some of which look very broad and very grey. They will be excluded if:

- they are or were a civil servant (or contracted to work in the government) and got the information while they were employed

- they are the taxpayer involved in the tax evasion or avoidance, or they planned and started the actions that led to the tax evasion or avoidance

- the information they provide may already be known to HMRC or could have been identified through routine processes

- the reward might directly or indirectly lead to funding illegal activity

- they are required by law to disclose, or not disclose, the information

- they are acting on behalf of someone else

- they got the information from someone who would not have been eligible for a reward themselves

- they are providing the information anonymously

Even if those tests are met, all and any payments and the level of such payments will also still be at HMRC’s discretion. Accordingly, it is highly questionable whether the scheme will be successful in achieving its stated aims to encourage well placed individuals who wouldn’t otherwise have come forward to approach HMRC with details of major tax evasion or aggressive failed tax avoidance. In fact, it seems that now we have the details – which have clearly been drawn up to be subject to the constraints of UK law as well as the constraints of the UK political environment and UK civil service culture – the scheme is highly likely to fail.

-

Loan charge review

Budget Day saw the publication of the outcome of the latest disguised remuneration loan charge review together with the publication of the Government’s detailed response – which accepted eight out of nine of the recommendations. Although taxpayers and advisors have in the past been cautioned not expect any major changes of policy to come out of the latest review and for it largely to be focused on fair time to pay arrangements, in the event the review has delivered radically improved outcomes for people who have yet to settle including:

- late payment interest will no longer be charged;

- penalties will never be sought;

- IHT will no longer be sought for arrangements involving trusts – the legitimate substantive nature of which was often questionable;

- a discount on the tax liabilities of out to £10,000 per year will be available in respect of historic promoter fees;

- repayment terms of up to five years available without having to discuss affordability;

- maximum reductions of up to £70,000 on what was payable under the loan charge (ignoring IHT for which no maximum waiver).

The only rejected recommendation was that any unpaid liabilities be written off after ten years. However, the government has instead decided to set no maximum duration over which repayments can be made

The new settlement terms will be formalised within Finance Bill 2025/26.

Although the terms are only stated to apply to taxpayers who have yet to settle and fall within the scope of the loan charge rather than other “pre loan charge” charging provisions that might be open to HMRC where it has open enquiries into particular years, obvious questions of fairness now arise for other parties. For instance, what of all the taxpayers who have previously agreed to pay IHT on trust arrangements which lacked genuine substance or have otherwise settled on less favourable terms? It seems the saga may yet rumble on before all serious unfairness is resolved.

More investigators investing small businesses

A further 350 investigators will be recruited and tasked with investigating the sort of small businesses which are believed by HMRC to make up over 60% of the UK’s tax compliance gap. Contrary to the headline Budget policy announcement, it is now understood that not all of them will be criminal investigators – but, nonetheless, increasing the number of criminal investigations will be part of the main focus.

Changes to penalty regime

With effect from 1 April 2026, company late filing fixed penalties will double – beginning with an initial fine of £200 – through to £2,000 fines where three successive failures occur where returns are more than three months late.

HMRC initiatives and new legislation

-

New nudge letters

HMRC issued a raft of new nudge letters in November including:

- Letters to UK holding companies of overseas subsidiaries claiming management expenses referring them to the relevant guidance on whether such expenses are allowable.

2. Letters to individuals who HMRC believe should have paid the remittance basis charge in 2023/24 under the UK’s outgoing non-dom regime.

3. Letters from HMRC’s Wealthy team reminding individuals of the rules for claiming foreign tax credits on overseas investment income or overseas employment income.

4. Letters from HMRC’s Wealthy team to people with income of more than £200,000 who failed to file tax returns in 2022/23.

5. Letters to companies which may have claimed excessive relief from S455 tax by making claims based on anticipated future repayment dates for director or participator loans.

As ever, all the letters put the onus on the taxpayers concerned to check their positions and make voluntary disclosures of any irregularities with the implicit threat of investigation hanging over them should they fail to do so.

What happened in October 2025

HMRC Initiatives and New Legislation

- HMRC launches new “customised journeys” to guide taxpayers during compliance checks

New online tools went live from HMRC to provide “customers” with more tailored journeys providing relevant guidance and explanatory videos when they come under investigation – for instance, advice on how to contest HMRC decisions or information notices. Inevitably, that guidance is still basic, not at all impartial and would be a very poor substitute for seeking professional help.

Case Decisions

- Mainpay Ltd v HMRC [2025] EWCA Civ 1290

The latest decision handed down by the Court of Appeal in this saga involving travel and subsistence payments made by an umbrella company to its temporary workers dismissed Mainpay’s appeal and found for HMRC.

The company reimbursed its temporary workers for these expenses using benchmark scale rates. It argued that these were deductible because the workers were employed under a single overarching employment contract, making each assignment a temporary workplace for the purposes of the legislation.

The Court endorsed the previous decisions of the First-Tier and Upper Tribunals in rejecting Mainpay’s argument that there was a single overarching or “discontinuous” employment contract.

It held that:

- Each assignment was a separate employment.

- Therefore, each workplace was a permanent workplace for tax purposes.

- As a result, travel and subsistence expenses were not deductible under sections 338–339 of ITEPA 2003.

The Court also confirmed that:

- There was no need to even consider whether benchmark scale rates could be used, since the expenses weren’t deductible in the first place.

- HMRC was entitled to extend assessment time limits due to carelessness by Mainpay, even though it had taken legal advice because the advice it relied upon came from lawyers who were not tax specialists and lacked a full understanding of the tax implications of employment arrangements. The failure to take proper advice was sufficient to meet the threshold for carelessness.

Why this matters

The ruling reinforces that umbrella companies must ensure their employment contracts are genuinely overarching if they wish to treat assignments as temporary workplaces.

It also makes clear that carelessness can be found even where professional advice was taken, if that advice was inadequate. In such circumstances, the taxpayer has a responsibility to ensure that they take tailored advice from suitably specialist and ostensibly competent advisers in the relevant area.

Other News and Announcements

- Capital Gains Tax investigations

Information obtained with a Freedom of Information (“FoI”) request by law firm BCLP show that HMRC recovered over £1/4billion in unpaid Capital Gains Tax in 2024/25 – up 41% on the year before as the number of related compliance checks increased to over 10,000 from less than 8,000 the year before.

Commenting on the increase in The Times, Price Bailey’s Andrew Park speculated that the increase was likely to relate in large part to HMRC’s crackdown down on undisclosed real estate gains and the increased proficiency with which HMRC now checks Land Registry records against personal tax returns.

- Crypto Tax investigations

An FoI request from UHY Hacker Young shows that HMRC is escalating its campaign to identify non-compliant crypto investors. HMRC sent nearly 65,000 nudge letters to crypto investors in 2024/25 – up from less than 28,000 in 2023/24 and none in 2022/23 after initial an initial drive in 2021/22 upon HMRC and international counterparts obtaining data from the Coinbase exchange.

HMRC’s efforts are set to escalate further when jurisdictions around the world begin the compulsory collection and exchange of data under the OECD led Crypto-Assets Reporting Framework.

Speaking to the Financial Times, Price Bailey’s Andrew Park explained that these developments were always inevitable after years of close work between HMRC and other tax authorities to obtain and exchange data. He added that: “Many taxpayers will have realised very large gains and will have big tax bills. However, many others will have realised large losses too and it will be crucial for them to have retained or have access to good records for them to be able to claim those losses and offset them against any gains”. He also emphasised the need for anyone who has bought and sold crypto assets – including exchanging cryptocurrency for other assets – to take urgent professional advice if there is a possibility that they are not take compliant – “unprompted disclosures attract a more benign treatment from HMRC – including lower penalties.”

- Increasing investigations into football clubs

Further FoI data shows that HMRC’s scrutiny of the professional football sector has intensified, with £90 million in extra tax recovered from clubs, players, and agents in the year to 31 March 2025—a 33% increase on the previous year. This uptick is the result of a more aggressive approach by HMRC, which has opened investigations into 12 clubs, 90 players and 16 agents over the period.

It is clear that HMRC now views football as a target rich environment in the pursuit of unpaid tax. HMRC has particular focus on:

- Research & Development (“R&D”) Tax Relief: Clubs have been claiming R&D relief for projects such as performance analytics and sports science. HMRC takes a dim view of the likelihood that football clubs are really seeking to make genuine scientific advances and, as with all R&D claimants, clubs must be prepared to justify claims with robust evidence of the projects they have undertaken and the credentials of the “competent professionals” they have relied upon to determine the scientific advances that would be made.

- Agent Fees and Dual-Representation Contracts: New HMRC guidelines mean that if a club claims an agent represented both the club and the player, it must provide clear evidence. Otherwise, the full fee is treated as paid by the player and subject to Income Tax.

HMRC also continues to pursue ex-professionals for unpaid tax from old investment schemes and failed tax avoidance arrangements.

The message for the football sector is clear. Clubs, players and agents should enter into no tax arrangements that will not bear close HMRC scrutiny and they should get specialist advice from reputable mainstream accountancy and law firms rather than tax avoidance boutiques selling artificial schemes.

What happened in September 2025

Contentious Tax Roundup – What happened in September 2025

In the September 2025 bulletin, Andrew Park, Tax Investigations Partner at Price Bailey, provides an overview of some of the most recent and significant contentious tax news, legislative changes, updates, and relevant case decisions that occurred throughout the month.

HMRC initiatives and new legislation

-

Nudge letter campaign aimed at VAT claimed by facilities management companies

Further to HMRC identifying that many facilities management companies are wrongly claiming input VAT on utility supplies purchased on behalf of their customers, HMRC has launched a new letter campaign requesting that such companies review their arrangements and respond to their HMRC customer compliance manager within 60 days confirming that they have reviewed their contracts and invoices and will take steps to rectify errors – or else, that they are satisfied that they have no errors to correct.

As with nudge letters in general, although they do not carry any legal force a failure to engage with them may result in investigation and may lead to harsher penalties in the event errors come to light.

A copy of the letter template is available here: OTM Final Letter

Case decisions

-

Ahmed & Ors v White & Company (UK) Ltd & Anor[2025] EWHC 2399 (Comm)

In a significant High Court decision on September 22, 2025, the court considered a professional indemnity claim involving 176 claimants who sued the now-liquidated accounting firm White & Co and its insurer, Allianz Global Corporate & Specialty SE (“Allianz”), over losses from failed tax-driven investments – including Enterprise Investment Schemes (EIS), Seed EIS, Super EIS, Films Rights Business (FRB), shares in DJI Holdings plc, Ober Private Clients Ltd, and corporate bonds. Many of these investments were promoted for their tax relief benefits, but ultimately failed.

The case focused on how White & Co’s notifications to Allianz were handled and how the policy terms should be interpreted in the context of:

- Negligent advice: The claimants alleged they received negligent and/or fraudulent advice from White & Co regarding high-risk tax-driven investment schemes.

- Company failure: White & Co went into administration in 2019 and was later liquidated. The claimants pursued compensation directly from the firm’s professional indemnity insurer, Allianz.

- The policy conditions: The core of the dispute focused on the terms of the Allianz insurance policy, which was active from November 2016 to December 2017. Key policy conditions included:

- Notification of circumstances: A requirement to promptly notify the insurer of any “circumstance… reasonably expected to give rise to a Claim”.

- Aggregation of claims: A provision existed to treat all related claims arising from the “same facts or alleged facts, or circumstances or the same Wrongful Act” as a single claim, with a corresponding financial limit.

- Tax Mitigation Endorsement: A clause capping the insurer’s liability for all claims related to “Tax Mitigation Schemes” at £2 million. These schemes were defined as pre-planned artificial transactions designed for a specific tax outcome.

The Court found that:

- Notification of claims: Several communications relied upon by the claimants, including specific letters and broader “Block Notifications,” were either insufficient to trigger coverage for the range of claims or were directed to an entity other than White & Co. The Court rejected the argument that broad communications constituted a “Hornet’s Nest” notification covering all potential claims.

- Aggregation of claims: Applying principles that aggregation clauses must be read against the specific policy wording, the court determined that the claims related to EIS, Seed EIS, and Super EIS investments were sufficiently similar to be aggregated into a single claim. This meant they would be subject to a single £2m financial limit under the policy.

- Tax Mitigation Endorsement: The court ruled that the policy’s Tax Mitigation Endorsement applied to advice on the sampled EIS, Seed EIS, Super EIS, and Film Rights Business investments, effectively capping Allianz’s total liability for these schemes.

Why this matters

The ruling provides important clarifications for the insurance and financial sectors on the interpretation of policy terms, particularly concerning notification, aggregation, and tax mitigation clauses.

The case underscores that:

- Emphasis on policy wording: The drafting and interpreting of policy language related to notification, aggregation, and specific exclusions is critically important. Insurers can rely on clear wording to aggregate large numbers of related claims, limiting their total exposure.

- Burden of notification: The burden lies with the insured (or claimants acting on their behalf) to provide unambiguous notification that complies with the specific requirements of the policy. Notifications must clearly detail the circumstances and relate to the correct insured party.

- Impact on professional indemnity: For financial advisors and other professionals, the decision highlights the need for a robust and timely notification process when problems with investments or advice emerge. The failure to do so can prevent compensation claims from being paid and can leave them with far greater uninsured exposure.

Other news and announcements

-

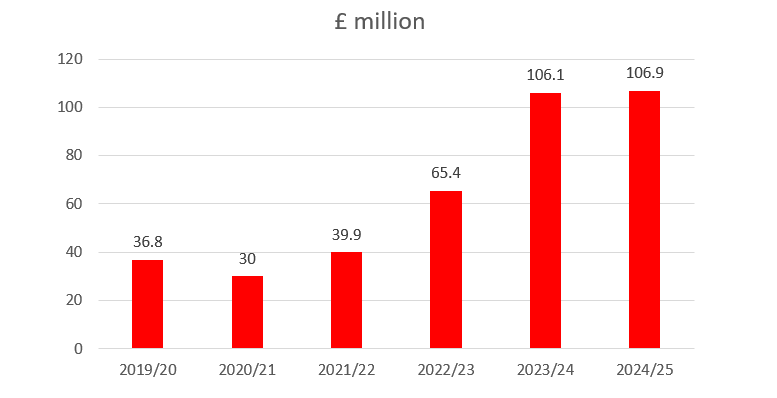

Price Bailey Freedom of Information (“FoI”) request reveals scale of HMRC offensive against non-compliant landlords

HMRC netted a record £107m from compliance activity targeting landlords in 2024/25, more than double the amount clawed in in 2021/22, according to data released to Price Bailey.

HMRC compliance yield from landlords

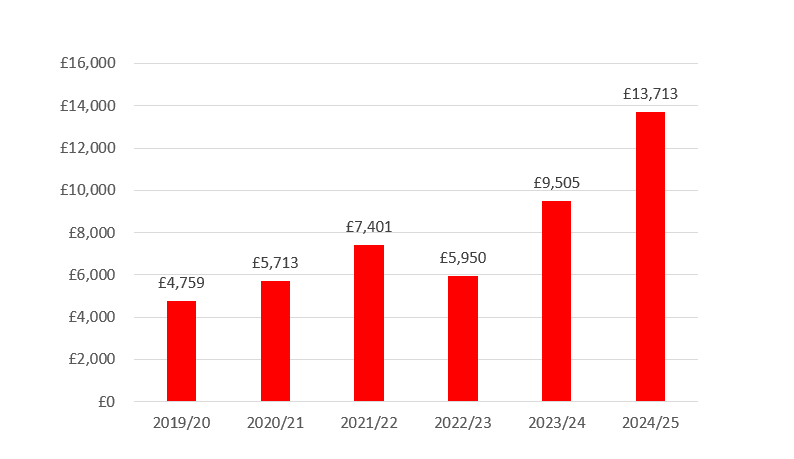

The Let Property Campaign (LPC), which was launched in the 2013/14 tax year, has brought in £570 million pounds in total from UK residential landlords. HMRC recovered £13,713 in tax per disclosure in 2024/25, by far the highest amount since the campaign’s inception.

Yield per disclosure under the Let Property Campaign

The data released under the FoI represents tax recovered from voluntary disclosures under the LPC, and from other connected compliance related activities, such as HMRC’s non-responder and discovery assessment work.

According to the Ministry of Housing, Communities & Local Government, there were about 2.2 million UK private landlords in the first quarter of 2024 (most recent estimate). There have been 100,332 disclosures so far under the LPC, representing just over four percent of the total population of UK landlords.

Speaking to the Telegraph, Andrew Park, Tax Investigations Partner at Price Bailey, commented:

We’ve assisted large numbers of landlords in making voluntary disclosures over the last few years – typically, after they’ve received an HMRC nudge letter.” He explained that there is, for instance, widespread confusion about the different tax treatment of capital expenditure and revenue expenditure. “Capital expenditure, such as installing a significantly upgraded kitchen, is not deductible against letting income, whereas repair and maintenance of an existing kitchen or a like-for-like replacement is deductible. That distinction can be grey around the edges and trips a lot of landlords up.

Often people are accidental landlords who kept a property after moving to cohabit with a new partner, inherited a property or temporarily moved abroad. Many are not financially sophisticated or in receipt of high levels of other income, haven’t properly understood their responsibilities and haven’t previously sought advice. It doesn’t help that many landlords have unexpected taxable profits on paper but only because tax law has now changed to ignore the full cost of debt servicing. This creates a “phantom profit” effect: landlords owe tax on deemed income that doesn’t economically exist.

The data serves to remind landlords that they should review their tax affairs carefully, especially if they have never sought advice or assumed no tax was due. In the event that omissions come to light it is never too late to make a voluntary disclosure to HMRC to mitigate the position.

What happened in August 2025

HMRC Initiatives and New Legislation

- New nudge letters targeting associated company arithmetic

In a campaign scheduled to run through until October 2025, HMRC has begun writing to companies it suspects of miscalculating their number of associated companies for Corporation Tax purposes, and resultantly claiming too much marginal relief.

HMRC is using two different letter types to test their comparative psychological effect on recipients – for instance, one is headed “Check . . .” and goes on to threaten a compliance check if ignored, and the other is headed “Please check . . .” and leaves the threat of investigation unspoken.

Copies of the alternative letters are available here:

This initiative further reflects the ever-increasing and imaginative breadth of HMRC’s use of “nudge letters” as well as HMRC’s increasingly sophisticated use of data from sources such as Companies House to trawl for potential anomalies. HMRC’s experimentation with language as a means of persuasion has been ongoing for c. 15 years, and the evolution of their “Jedi mind tricks” evidently still has some way to go.

- Self-serve time to pay extended to Simple Assessment debts

Should they need it, Agent Update 134 announces that taxpayers receiving Simple Assessment letters advising them of further liabilities payable within three months or by 31 January 2026 are now being given online access to set up payment plans.

To qualify, taxpayers must owe between £32 and £50,000 and not have any other payment plans in place with HMRC or have any other outstanding debts to HMRC.

Sums owed will, of course, be subject to HMRC’s newly increased and more punitive late payment interest set at Bank of England base plus 4%.

Notably, tax is not deducted at source from the UK State Pension and Simple Assessments are issued after the tax year to pensioners in the event that they receive more State Pension than their personal allowance and do not have other work or private pension income from which the tax can be taken under PAYE and are not otherwise filing tax returns. The surge in the State Pension under the “Triple Lock” and frozen personal allowances will result in huge numbers of impoverished pensioners getting a nasty shock through their letterbox in this regard. A few hundred pounds is a lot of money to somebody who doesn’t have any. So, it seems likely that HMRC has extended easy access to time to pay very much with this in mind.

Case Decisions

- Lexgreen Services v HMRC [2025] UKFTT 1019 (TC)

“This is a case about the meaning of life” – so begins the Judge’s decision in this case before the First-tier Tax Tribunal (“FTT”) . . .

More specifically, the case concerns whether a corporate settlor was liable for Inheritance Tax (“IHT”) upon the 10-year anniversary of the settlement of a remuneration trust in 2005 under the provisions of the S201(d) Inheritance Tax Act 1984 – that provision applying where

where: “. . . the transfer is made during the life of the settlor . . .”.

Acting for the Appellant, Michael Firth KC argued that the legislation does not and was not intended to encompass corporate settlors or else it would have been drafted differently – that IHT is fundamentally concerned with life and death, a company has no life force and cannot make a transfer during its life as a settlor – “life” should have its ordinary meaning i.e. the period between birth and death of a living thing. The Court disagreed and found that the company was a live company at all material times – had the parliamentary draftsman intended to exclude corporate settlors from the application of the provision and limit it to “natural settlors”, it would have been a simple matter to do so.

Why this matters

This case involves a Baxendale Walker promoted tax avoidance arrangement and was designated a lead case to determine the same issue for a group of other cases under appeal, which depend upon the same principle. Had the Court found in the Appellant’s favour, it would have had wider ramifications for those other appeals and for many other longstanding trust arrangements involving corporate settlors. Ultimately, although argued for the Appellant with flair, the purposive approach adopted by the Court and the outcome was always the most likely outcome. The Courts now place little reliance on literal interpretation and tend these days to have more of an eye on what they feel the Law should be, even if the legislation doesn’t always articulate it very well.

- Elsbury v Information Commissioner [2025] UKFTT 915 (GRC)

In this unusual case before the First-Tier Tribunal (General Regulatory Chamber) Information Rights (“GRC”), the Appellant sought to compel HMRC to comply with a Freedom of Information (“FoI”) request to provide details of whether HMRC uses artificial intelligence (“AI”) in deciding whether or not to accept claims Research & Development (“R&D”) tax credits. Have HMRC been using AI to determine whether a projects truly aimed to achieve advances in science or technology and overcome uncertainties that “competent professionals” cannot readily simply deduce. It would be understandable if HMRC had started to move in that direction, given how ill-equipped its officers are to conclude on matters of science and technology that don’t fall within their experience, training or intellectual grasp. However, the Appellant has major concerns that patterns show HMRC is both using AI and still coming to inappropriate generic conclusions.

HMRC had refused the FoI on the basis that it would prejudice the collection of tax, and the Information Commissioner – who was the Respondent here rather than HMRC – had found for HMRC. However, the GRC has now overturned this on the basis that the public interest in transparency outweighs HMRC’s objections. HMRC now has until 18 September 2025 to reveal the information.

Why this matters

This is a rare instance of HMRC’s refusal to provide FoI information being challenged in the courts and challenged successfully. It will be fascinating to have an insight into whether and how HMRC has been using AI in such a high-activity area of contentious tax when HMRC’s response is made public. The answers may raise further questions and concerns.

It is also hoped that this reminder that there are limits to HMRC’s ability to refuse FoI requests when it suits them will lead to a greater volume of FoI data being released across the board.

Other News and Announcements

- Rt Hon Angela Rayner – SDLT investigation

The news about the Secretary of State for Housing, Communities and Local Government has failed to pay the right amount of SDLT on a property transaction and is now under HMRC investigation, serves as a salutary lesson on how complicated tax can be and the need to both seek advice from suitably specialist professional advisors and provide them with all of the necessary relevant information.

As many news reports highlighted, failure to get the tax bill right, resulting from carelessness, can result in penalties of up to 30% of the unpaid tax plus punitive late payment interest. Less well publicised was the possibility that in some circumstances – seemingly not those relating to Ms Rayner – HMRC and the Courts can view any wilful negligence in failing to get proper advice for fear of what that advice might be (so-called “Nelsonian blindness”) to be deliberate wrongdoing which can attract much higher penalties still.

What happened in July 2025

In the July contentious tax bulletin, Andrew Park, Tax Investigations Partner at Price Bailey, provides an overview of the most recent and significant contentious tax news, legislative changes, updates, and relevant case decisions that occurred throughout the previous month.

HMRC initiatives and new legislation

-

HMRC’s transformation roadmap

HMRC published a new “roadmap” on 21 July 2025. Alongside other objectives like improving the so-called “customer experience”, a core central element of the roadmap is HMRC’s strategy for “closing the tax gap” i.e. reducing the amount of tax – currently estimated at c. £47bn – which is payable under the law but which goes uncollected.

HMRC plans to improve compliance by:

- making increasing use of digitisation and AI to gather and analyse data to pre-populate entries in returns, identify taxpayers who need to brought within the system and send even greater numbers of “nudge letters” to taxpayers who appear to be non-compliant;

- improving IT systems to enable better real-time reporting and communication;

- bringing in new legislation from April 2026 to make recruitment companies that use umbrella companies legally responsible for accounting for PAYE on workers’ pay;

- targeting rogue tax advisors with enhanced information gathering powers and sanctions;

- modernising systems and processes for debt collection;

- aiming to increase the number of criminal prosecutions by 20% over the next five years;

- launching the already announced new HMRC whistleblower reward scheme by late 2025;

- recruiting c. 400 people – including external tax professionals – to bolster HMRC Fraud investigation Service’s efforts to tackle serious offshore non-compliance by the wealthy.

Case decisions

-

Marlborough DP Ltd v HMRC [2025] EWCA Civ 796

This case heard by Court of Appeal revolved around a tax avoidance scheme involving a dental practice company, Marlborough DP Ltd (“MDPL”), and its sole director and owner, Dr Matthew Thomas. The company had paid nearly all its annual profits into an offshore Remuneration Trust (“RT”), which then loaned back matching amounts to Dr Thomas. The scheme – which had been designed by the infamous Paul Baxendale-Walker (aka Paul Chaplin) – aimed to secure a Corporation Tax deduction for the contributions and deliver untaxed cash to Dr Thomas as loans rather than employment earnings or shareholder dividends.